EMIs Demystified: Everything You Need to Know

Last Updated : June 2, 2025, 5:27 p.m.

Equated Monthly Installments (EMIs) are a cornerstone of loan repayment in India, whether you’re financing a home, car, or personal expenses. Understanding EMIs can help you plan your finances better and avoid repayment stress. In this comprehensive guide, Wishfin breaks down everything you need to know about EMIs, from how they work to tips for managing them effectively.

What Is an EMI?

An EMI, or Equated Monthly Installment, is a fixed monthly payment made to repay a loan over a specified period. It includes both the principal amount and the interest charged by the lender. EMIs are common for financial products like home loans , personal loans, car loans, and credit card dues.

How Does an EMI Work?

EMIs are calculated based on three key factors:

- Loan Amount: The total amount borrowed.

- Interest Rate: The rate charged by the lender, which can be fixed or floating.

- Loan Tenure: The duration over which the loan is repaid (e.g., 5, 10, or 20 years).

The EMI formula is:

EMI = [P x R x (1+R)^N] / [(1+R)^N - 1]

Where:

- P = Principal loan amount

- R = Monthly interest rate (annual rate / 12)

- N = Number of monthly installments

Instead of manual calculations, you can use Wishfin’s EMI calculator to get accurate EMI estimates instantly.

Components of an EMI

Each EMI payment consists of two parts:

- Principal: The portion that reduces the outstanding loan amount.

- Interest: The cost of borrowing, paid to the lender.

In the early stages of a loan, the interest component is higher, while the principal component increases over time. This is known as the amortization schedule.

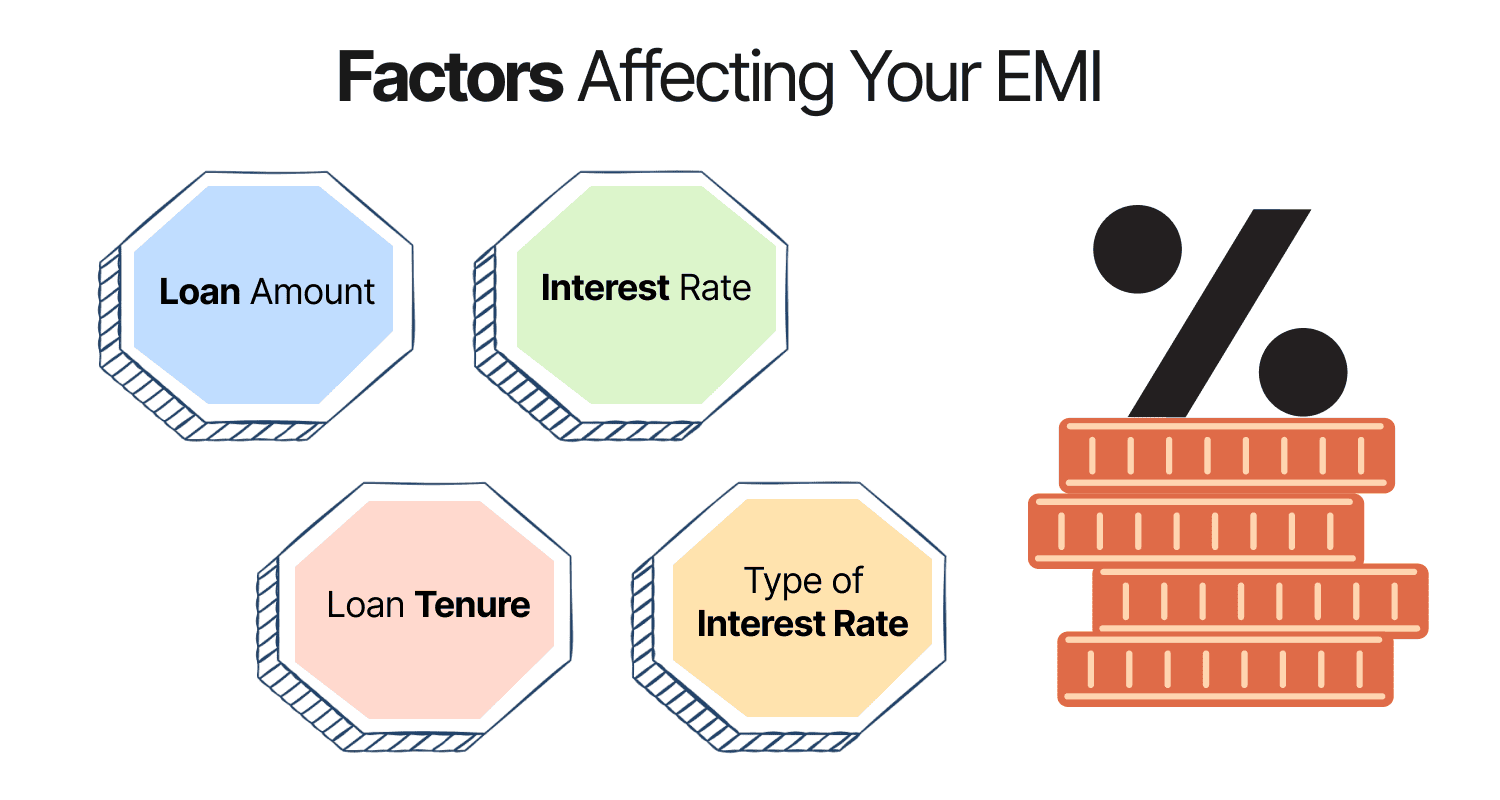

Factors Affecting Your EMI

1. Loan Amount

A higher loan amount increases your EMI. For example, borrowing ₹50 lakh for a home loan will result in a higher EMI than borrowing ₹20 lakh.

2. Interest Rate

Higher interest rates lead to higher EMIs. For instance, personal loans (10-24% p.a.) typically have higher EMIs than home loans (8-10% p.a.).

3. Loan Tenure

Longer tenures reduce monthly EMIs but increase the total interest paid. Shorter tenures mean higher EMIs but lower overall interest.

4. Type of Interest Rate

- Fixed Rate: EMIs remain constant throughout the loan tenure.

- Floating Rate: EMIs may vary based on market conditions or changes in the lender’s base rate.

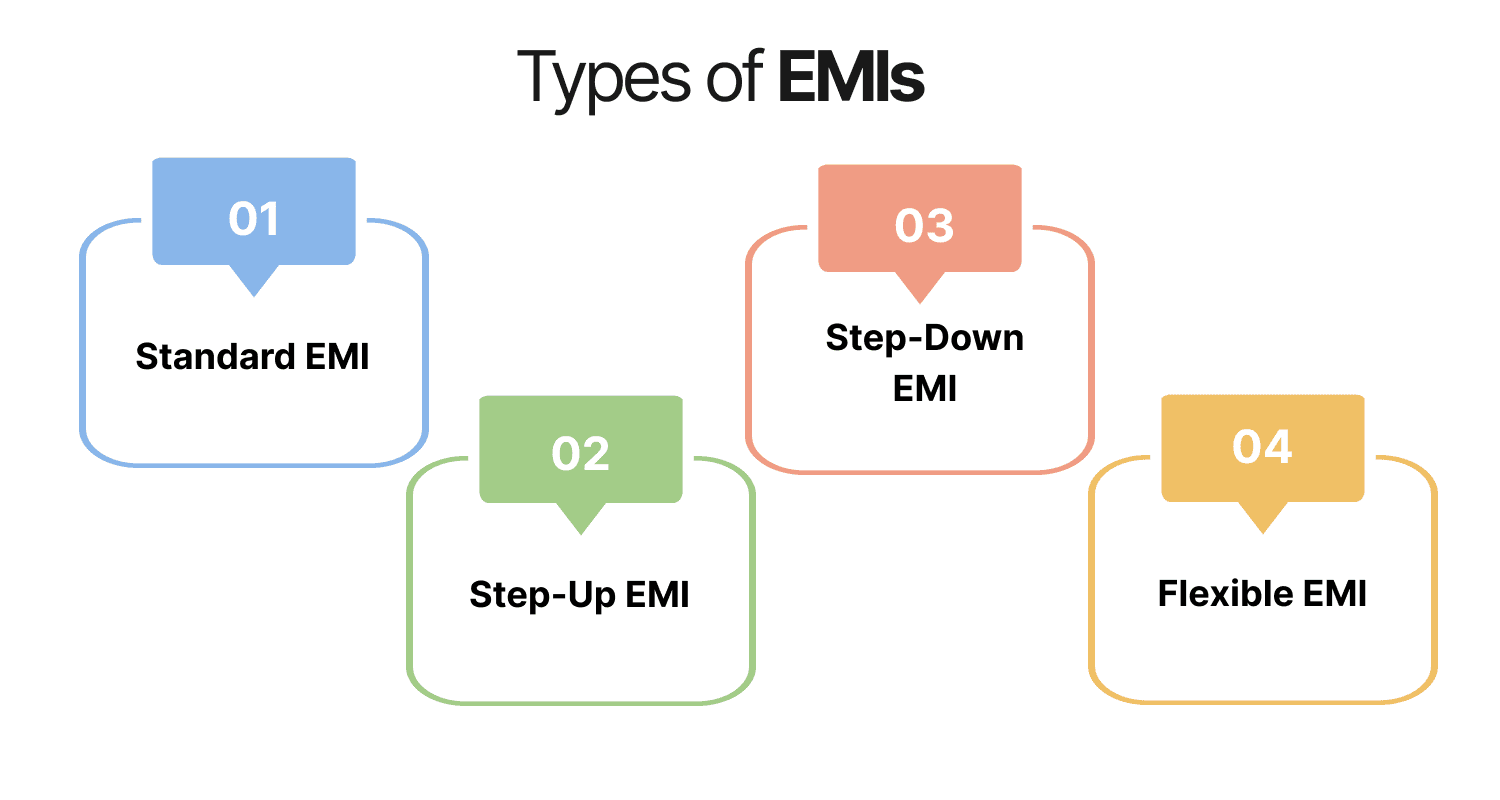

Types of EMIs

- Standard EMI: Fixed monthly payments for the entire tenure, common for home and car loans.

- Step-Up EMI: Starts with lower EMIs that increase over time, ideal for young professionals expecting income growth.

- Step-Down EMI: Higher EMIs initially that decrease over time, suitable for those nearing retirement.

- Flexible EMI: Allows occasional overpayments or underpayments, offered by select lenders.

How to Calculate Your EMI?

Calculating EMIs manually can be complex, but tools like Wishfin’s EMI calculator simplify the process. Just input:

- Loan amount

- Interest rate

- Tenure

The calculator provides your monthly EMI, total interest payable, and amortization schedule, helping you plan your finances.

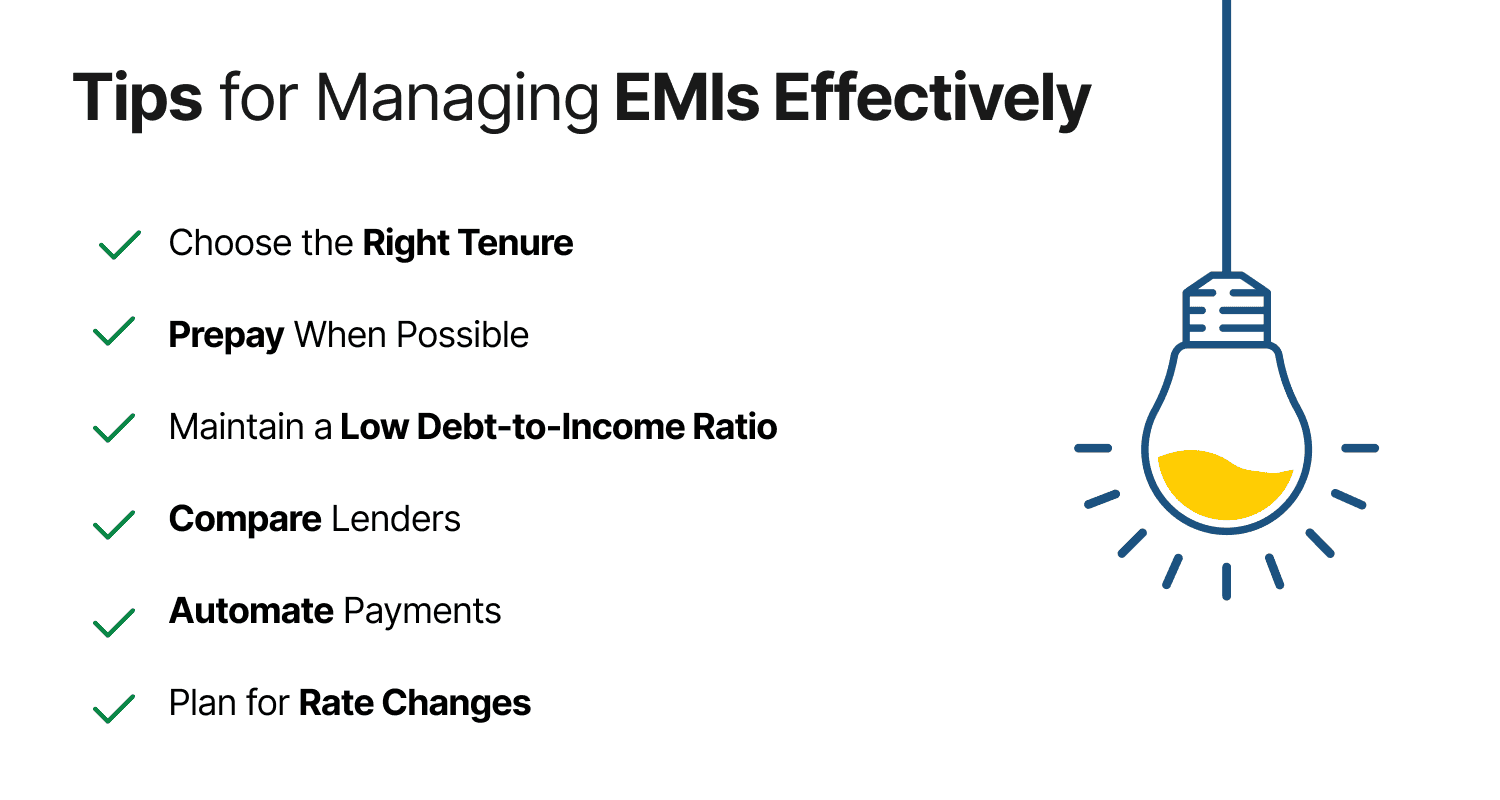

Tips for Managing EMIs Effectively

- Choose the Right Tenure: Opt for a tenure that balances affordable EMIs with lower total interest. Use Wishfin’s EMI calculator to compare options.

- Prepay When Possible: Making partial prepayments can reduce the principal, lowering either your EMI or tenure.

- Maintain a Low Debt-to-Income Ratio: Ensure your total EMI payments don’t exceed 40-50% of your monthly income to avoid financial strain.

- Compare Lenders: Different lenders offer varying interest rates and terms. Compare personal loans or home loans on Wishfin for the best deals.

- Automate Payments: Set up auto-debit to avoid missing EMI payments, which can harm your credit score.

- Plan for Rate Changes: If you have a floating-rate loan, budget for potential EMI increases due to market fluctuations.

Common EMI Myths Debunked

- Myth: Longer tenures always save money.

Fact: Longer tenures reduce EMIs but increase total interest paid. - Myth: EMIs are the same for all loan types.

Fact: EMIs vary based on loan type, interest rate, and tenure. - Myth: Prepayment always reduces EMIs.

Fact: Prepayment can reduce either the EMI or tenure, depending on the lender’s policy.

How Wishfin Can Help?

Wishfin makes EMI management easy with tools like the EMI calculator and loan comparison platform. Whether you’re applying for a home loan or personal loan, Wishfin helps you find lenders with the lowest rates and flexible terms, ensuring affordable EMIs tailored to your budget.

Conclusion

EMIs are a vital part of loan repayment, and understanding them can empower you to make smarter financial decisions. By grasping how EMIs are calculated, exploring different types, and following practical management tips, you can keep your finances on track. With Wishfin’s resources, you can compare loans, calculate EMIs, and choose the best repayment plan for your needs in 2025.

Frequently Asked Questions (FAQs)

What is an EMI, and how is it calculated?

Can I reduce my EMI after taking a loan?

How does loan tenure affect my EMI?

What happens if I miss an EMI payment?

How can Wishfin help me manage my EMIs?

Best Offers For You!

Personal Loan Rates by Top Banks

- HDFC Personal Loan Interest Rates

- ICICI Personal Loan Interest Rates

- Kotak Personal Loan Interest Rates

- IndusInd Bank Personal Loan Interest Rates

- RBL Bank Personal Loan Interest Rates

- YES BANK Personal Loan Interest Rates

- IDFC First Bank Personal Loan

- Tata Capital Personal Loan

- SMFG India Credit Personal Loan

- SCB Personal Loan Interest Rates

- SBI Personal Loan Interest Rates

- Axis Bank Personal Loan Interest Rates

Personal Loan

- Personal Loan

- Personal Loan Eligibility Calculator

- Personal Loan EMI Calculator

- Personal Loan Interest Rates

- Pre-approved Personal Loan in India

- Personal Loan Top Up in India

- Personal Loan Balance Transfer

- Apply Personal Loan on WhatsApp

- Personal Loan for Unemployed

- Personal Loan for Government Employees

- Personal Loan Without CIBIL Score

- Minimum CIBIL Score for Home Loan

Personal Loan Calculator by Top Banks

- HDFC Personal Loan EMI Calculator

- ICICI Personal Loan EMI Calculator

- Kotak Personal Loan EMI Calculator

- IndusInd Bank Personal Loan EMI Calculator

- RBL Bank Personal Loan EMI Calculator

- YES Bank Personal Loan EMI Calculator

- IDFC First Bank Personal Loan EMI Calculator

- Tata Capital Personal Loan EMI Calculator

- SMFG India Credit Personal Loan EMI Calculator

- Standard Chartered Personal Loan EMI Calculator

- SBI Personal Loan EMI Calculator

- Axis Bank Personal Loan EMI Calculator