Fixed vs Floating Interest Rate Loans: What’s Best in the Current Market?

Last Updated : June 4, 2025, 5:22 p.m.

India’s loan market in 2025 is booming. From home loans to personal, education, and car loans, borrowers are prioritizing smart borrowing choices. A major decision today is choosing between fixed vs floating interest rate loans. This choice affects your EMIs, total interest, and overall financial strategy.

In this guide, we simplify both interest rate types, highlight current trends, and help you choose the most cost-effective option based on your income profile, loan tenure, and market expectations. If you're wondering which is better: fixed or floating interest rate loan in 2025, this article is for you.

What is a Fixed Interest Rate Loan?

A fixed interest rate loan has a persistent interest during the span of the loan. Your monthly EMI remains unchanged, regardless of repo rate fluctuations. Fixed rate loans in India provide stability and are often chosen by those looking to avoid future uncertainty.

Benefits:

- Predictable EMIs, easier budgeting

- Immunity from future rate hikes

- Financial certainty

Drawbacks:

- Typically higher than floating rates

- No gains if interest rates fall

- May include prepayment charges

Ideal for: Salaried borrowers, retirees, or those who want EMI stability.

What is a Floating Interest Rate Loan?

A floating interest rate loan shifts depending on external criteria like the RBI repo rate or MCLR. Floating rate loans are more popular when repo rates are trending downward.

Benefits:

- Lower starting rate

- EMI may reduce if rates fall

- Usually no prepayment penalties

Drawbacks:

- EMI may rise if rates increase

- Budgeting becomes unpredictable

- May extend loan tenure

Best suited for: Entrepreneurs, young professionals, or borrowers expecting higher future income.

Fixed vs Floating Loans: Comparison Table

| Feature | Fixed Rate Loan | Floating Rate Loan |

|---|---|---|

Interest Rate | Constant | Changes with market |

EMI | Fixed | Variable |

Initial Rate | Usually higher | Usually lower |

Risk Factor | Low | High |

Prepayment Charges | May apply | Usually none |

Suitable For | Risk-averse | Rate-sensitive borrowers |

Which is Better in 2026: Fixed or Floating?

With the RBI cutting rates to boost growth, floating interest rate loans in India have become more appealing in 2025. Lower entry rates and room for future reductions make them ideal for long-term borrowers looking to compare fixed and floating loans in India.

However, if you're worried about rate hikes or prefer stability, fixed vs floating interest rate loans may still lean in favor of fixed rates for short-term planning. This comparison of fixed vs floating interest rate loans in India helps borrowers make informed decisions based on their financial situation and loan goals.

Example:

- Salaried employee: Safer with fixed EMIs

- Young borrower: Floating may help build savings over time

Pro Tip: Use online EMI calculators to simulate both fixed and floating rate options in best- and worst-case scenarios.

Home Loans in 2025

Loan Tenure: 15–30 years

Recommendation: Floating rate home loans are ideal for long tenures

Choose fixed only if rising EMIs will strain your finances

SBI and HDFC offer repo-linked floating home loans from 8.35% p.a.

Fixed vs floating interest rate loans for home loans should be evaluated based on tenure and income certainty.

Car Loans

Tenure: 3–7 years

Short tenure (up to 3 years): Fixed is better

Longer tenure (5+ years): Floating is smarter in falling rate cycles

Bank of Baroda and other PSBs give floating rate car loans

Comparing fixed and floating car loans in India can help choose the right financing.

Education Loans

Tenure: 10–15 years

Most are floating, repo or MCLR-linked

Choose fixed if offered a special rate or if budgeting is a priority

SBI and Canara Bank offer education loans from 9.15% p.a. (floating)

Use EMI tools to evaluate the benefits of fixed vs floating interest rate structures.

Personal Loans

Duration: 1–5 years

Fixed personal loan rates give EMI certainty

Choose floating only for 4+ year terms and in falling repo cycles

NBFCs are gradually introducing floating personal loans

When choosing between fixed vs floating personal loans, tenure and market outlook are key.

Common Mistakes to Avoid

- Locking into fixed before a rate cut

- Ignoring prepayment clauses

- Taking floating loans without a financial buffer

- Skipping EMI simulations

- Assuming rates will always remain low

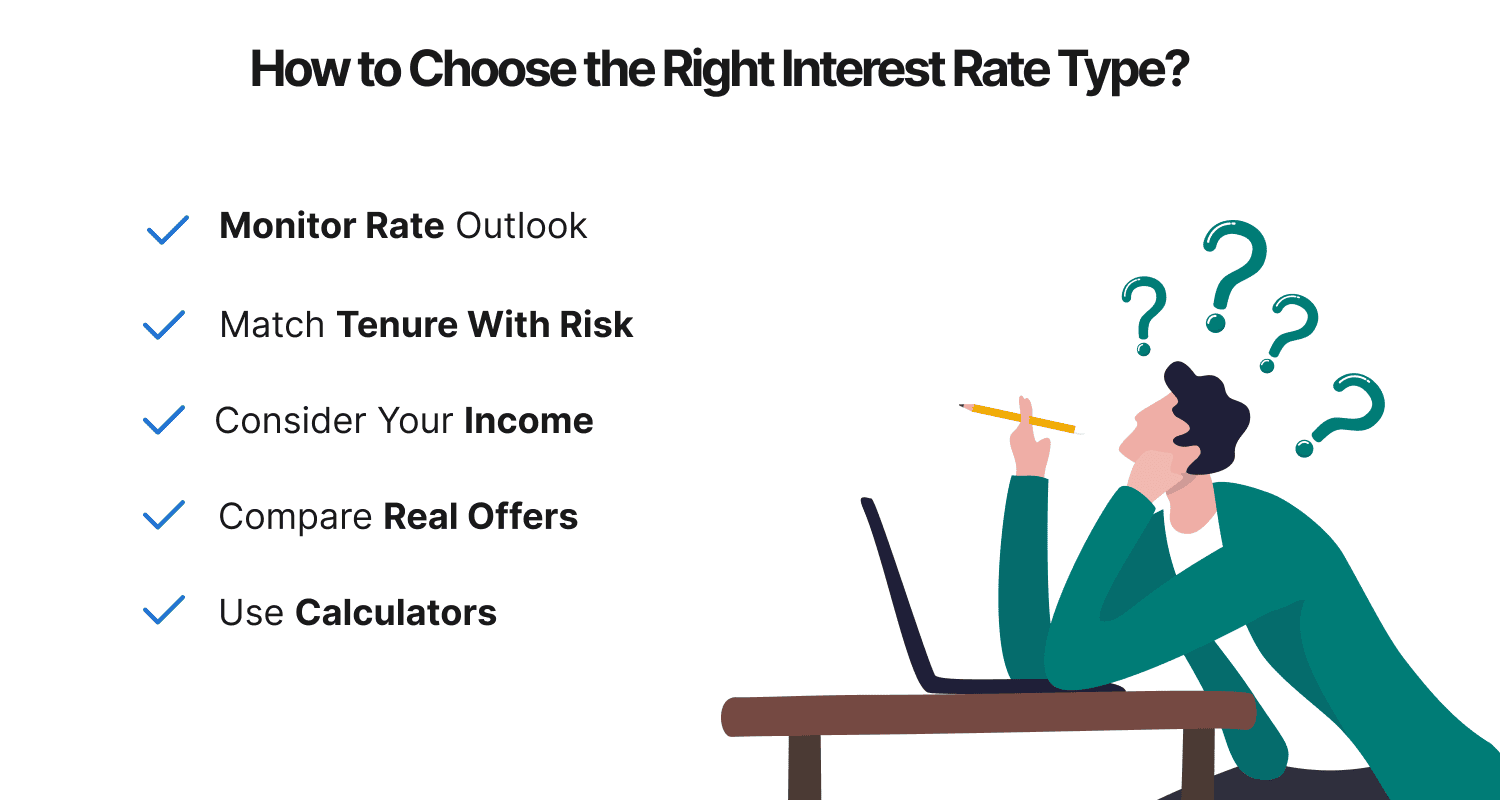

How to Choose the Right Interest Rate Type?

- Monitor rate outlook – Repo cuts favor floating, but cycles reverse

- Match tenure with risk – Short term = Fixed; Long term = Floating

- Consider your income – Stable = Fixed; Growing = Floating

- Compare real offers – Slightly higher fixed rate might be worth stability

- Use calculators – Evaluate best- and worst-case EMI scenarios

Conclusion

There’s no universal winner in the fixed vs floating interest rate loans debate. Your best option depends on market trends, loan duration, and personal finances. Understanding the benefits of fixed vs floating interest rate structures is crucial.

Choose floating rate loans if rates are expected to come down or for long-term borrowing. Pick fixed rate loans if you need predictability or are borrowing short-term.

Use Wishfin’s EMI calculators to make an informed decision.

Frequently Asked Questions (FAQs)

Which is better—fixed or floating rate for education loans?

Can I switch between fixed and floating later?

Who offers low floating rates in 2025?

Are fixed rate education loans available?

Do floating loans have prepayment penalties?

What happens if rates rise after I take a floating loan?

How to compare fixed and floating loans effectively?

Fixed or floating interest rate loans in 2025 - Which is better?

Best Offers For You!

Personal Loan Rates by Top Banks

- HDFC Personal Loan Interest Rates

- ICICI Personal Loan Interest Rates

- Kotak Personal Loan Interest Rates

- IndusInd Bank Personal Loan Interest Rates

- RBL Bank Personal Loan Interest Rates

- YES BANK Personal Loan Interest Rates

- IDFC First Bank Personal Loan

- Tata Capital Personal Loan

- SMFG India Credit Personal Loan

- SCB Personal Loan Interest Rates

- SBI Personal Loan Interest Rates

- Axis Bank Personal Loan Interest Rates

Personal Loan

- Personal Loan

- Personal Loan Eligibility Calculator

- Personal Loan EMI Calculator

- Personal Loan Interest Rates

- Pre-approved Personal Loan in India

- Personal Loan Top Up in India

- Personal Loan Balance Transfer

- Apply Personal Loan on WhatsApp

- Personal Loan for Unemployed

- Personal Loan for Government Employees

- Personal Loan Without CIBIL Score

- Minimum CIBIL Score for Home Loan

Personal Loan Calculator by Top Banks

- HDFC Personal Loan EMI Calculator

- ICICI Personal Loan EMI Calculator

- Kotak Personal Loan EMI Calculator

- IndusInd Bank Personal Loan EMI Calculator

- RBL Bank Personal Loan EMI Calculator

- YES Bank Personal Loan EMI Calculator

- IDFC First Bank Personal Loan EMI Calculator

- Tata Capital Personal Loan EMI Calculator

- SMFG India Credit Personal Loan EMI Calculator

- Standard Chartered Personal Loan EMI Calculator

- SBI Personal Loan EMI Calculator

- Axis Bank Personal Loan EMI Calculator