Best Banks in India for Saving Accounts

Last Updated : June 16, 2025, 6:41 p.m.

In 2025, India's banking sector will offer a dynamic range of savings accounts tailored to diverse financial needs, from high-yield options to zero-balance accounts . With robust digital platforms and extensive networks, the top banks blend innovation and accessibility. This article explores the best banks for savings accounts, guiding you to make informed choices based on interest rates, services, and reliability.

Top 10 Banks for Savings Accounts in 2026

| Bank Name | Interest Rate (p.a.) | Minimum Balance (INR) | Key Features |

|---|---|---|---|

HDFC Bank | 3.00% - 3.50% | Rural: 2,500; Semi-Urban: 5,000; Urban/Metro: 10,000 | 9,092 branches, 20,993 ATMs, MobileBanking app, free debit cards, women/senior accounts |

ICICI Bank | 3.00% - 3.50% | Rural: 1,000 (Gramin)/2,000; Semi-Urban: 5,000; Urban/Metro: 10,000 | iMobile Pay app, 6,613 branches, 16,120 ATMs, instant virtual debit card, 250+ services |

State Bank of India (SBI) | 2.70% - 3.00% | Nil (zero-balance account) | 22,500+ branches, 60,000+ ATMs, YONO app, auto-sweep facility, no MAB penalty |

Kotak Mahindra Bank | 3.50% - 4.00% | Varies: 2,500 - 50,000 (by account type) | 811 Edge digital account, instant online opening, discounts on shopping/travel |

Axis Bank | 3.00% - 3.50% (< ₹800Cr) | Rural: 2,500; Semi-Urban: 5,000; Urban/Metro: 12,000 | 15% cashback on Amazon/Flipkart, extensive ATM network, digital wallets |

IndusInd Bank | 3.00% - 7.00% | Varies: Nil - 20,000 (by account type) | 15+ account variants, 3-in-1 trading account, free NEFT/RTGS/IMPS |

Yes Bank | 3.00% - 7.00% | 10,000 | Customizable accounts, zero forex debit cards, up to 500 reward points on opening |

IDFC FIRST Bank | 3.00% - 7.00% | 10,000 or 25,000 (choice) | Monthly interest credits, zero-fee banking (NEFT/RTGS/IMPS), advanced mobile app |

AU Small Finance Bank | 3.00% - 7.25% | Zero Balance | High interest rates, free digital transactions, 25% off Swiggy, rural focus |

RBL Bank | 3.50% - 7.50% | Varies: 5,000 - 50,000 (by account type) | High interest rates, locker benefits, choose-your-account-number feature |

Why Choose These Banks?

- Private Banks (HDFC, ICICI, Kotak, Axis, Yes, IDFC FIRST, AU, RBL, IndusInd) : These banks lead in digital innovation, offering user-friendly apps, instant account opening via e-KYC, and higher interest rates (up to 7.50% p.a.). They cater to urban customers with premium services like cashback, zero forex debit cards, and personalized accounts for women or seniors. However, they often require higher minimum balances in metro areas (e.g., ₹10,000-₹12,000).

- Public Sector Bank (SBI) : SBI stands out for its unmatched branch/ATM network, zero-balance accounts, and financial inclusion focus, making it ideal for rural customers and those prioritizing accessibility. Its lower interest rates (2.70%-3.00%) are offset by reliability and government backing.

- Small Finance Bank (AU) : AU Small Finance Bank offers high interest rates (up to 7.25%) and zero-balance accounts, appealing to savers seeking maximum returns with minimal requirements.

Things to Consider While Opening a Savings Bank Account

- Interest Rates

- Why It Matters : Higher interest rates increase your savings growth over time.

- Details : Rates range from 2.70% (e.g., SBI) to 8.00% p.a. (e.g., ESAF Small Finance Bank). Small finance banks like AU (up to 7.25%) and RBL (up to 7.50%) offer higher rates for larger balances, while larger banks like HDFC and ICICI provide 3.00%-3.50%.

- Consideration : Check balance slabs, as rates often increase with higher deposits (e.g., IDFC FIRST offers 7.00% for balances above ₹1 lakh). Choose a bank with competitive rates if maximizing returns is a priority.

- Minimum Balance Requirements

- Why It Matters : Failing to maintain the minimum balance can lead to penalties, reducing your savings.

- Details : Varies by bank and location—SBI and AU Small Finance Bank offer zero-balance accounts, while HDFC requires ₹10,000 in urban/metro areas and ICICI ₹5,000 in semi-urban areas. Small finance banks like Equitas may require ₹2,500 (assumed).

- Consideration : Opt for zero-balance accounts if you have irregular income or prefer flexibility, especially for students or rural customers.

- Branch and ATM Network

- Why It Matters : A wide network ensures easy access to cash withdrawals and in-person services.

- Details : SBI leads with 22,500+ branches and 60,000+ ATMs, ideal for rural areas. Private banks like HDFC (9,092 branches, 20,993 ATMs) and ICICI (6,613 branches, 16,120 ATMs) focus on urban centres. Small finance banks have fewer branches.

- Consideration : Choose a bank with a strong local presence if you rely on physical banking; urban users may prioritize banks with extensive ATM networks to avoid fees.

- Digital Banking Capabilities

- Why It Matters : Online and mobile banking simplify transactions, bill payments, and account management.

- Details : Private banks like ICICI (iMobile Pay), Kotak (811 Edge), and IDFC FIRST (zero-fee transactions) offer advanced apps. SBI’s YONO is improving but less seamless. Features include UPI, WhatsApp banking (Yes Bank), and expense tracking.

- Consideration : Select a bank with a user-friendly app if you prefer managing finances digitally, especially for frequent online transactions.

- Customer Service

- Why It Matters : Reliable support ensures quick resolution of issues like transaction disputes or account queries.

- Details : Private banks like HDFC, Axis, and Kotak are highly rated for urban service, with fast response times. SBI excels in rural areas but varies by branch.

- Consideration : Review customer feedback on platforms like MouthShut or Google Reviews to assess service quality, particularly for your region.

- Additional Features and Benefits

- Why It Matters : Extra perks enhance the account’s value and align with your lifestyle.

- Details : Examples include cashback (Axis: 15% on Amazon/Flipkart), zero forex debit cards (RBL), monthly interest credits (IDFC FIRST), and discounts (AU: 25% off Swiggy). Specialized accounts for women (ICICI) or seniors (SBI) offer tailored benefits.

- Consideration : Look for features like reward points, free insurance, or locker discounts that match your spending habits or needs.

- Fees and Charges

- Why It Matters : Hidden fees can erode your savings, especially for frequent transactions or non-maintenance of minimum balance.

- Details : HDFC charges ₹600/quarter for non-maintenance in urban areas, while IDFC FIRST offers zero fees for NEFT/RTGS/IMPS. SBI has no minimum balance penalties. ATM withdrawal fees vary (e.g., 5 free non-DCB ATM withdrawals at DCB Bank).

- Consideration : Compare charges for digital transactions, ATM usage, and penalties to minimize costs, especially if you transact frequently.

- Financial Stability and Safety

- Why It Matters : Ensures your deposits are secure and the bank is trustworthy.

- Details : All RBI-regulated banks (public, private, small finance) insure deposits up to ₹5 lakh via DICGC. Public banks like SBI are government-backed, while private banks like HDFC (₹14.8 lakh crore market cap) and ICICI (₹8.73 lakh crore) are financially robust.

- Consideration : Choose a bank with a strong track record and RBI oversight for peace of mind, particularly for large savings.

- Account Opening Process

- Why It Matters : A seamless onboarding process saves time and effort.

- Details : Private banks like Kotak (811 Digital), IDFC FIRST, and Yes Bank offer instant online opening via e-KYC. SBI’s YONO supports digital opening, but some public banks (e.g., Bank of Baroda) may require branch visits.

- Consideration : Opt for fully digital onboarding if convenience is key; verify KYC requirements (Aadhaar, PAN) in advance.

- Accessibility and Financial Inclusion

- Why It Matters : Ensures banking services are available to all, especially in underserved areas or for specific groups.

- Details : SBI and public banks prioritize rural outreach with zero-balance accounts. Small finance banks like AU and ESAF focus on low-income households. Accounts for women (ICICI), seniors (SBI), or students (Kotak) cater to niche needs.

- Consideration : Choose banks with inclusive offerings if you’re in a rural area, have low income, or belong to a specific demographic.

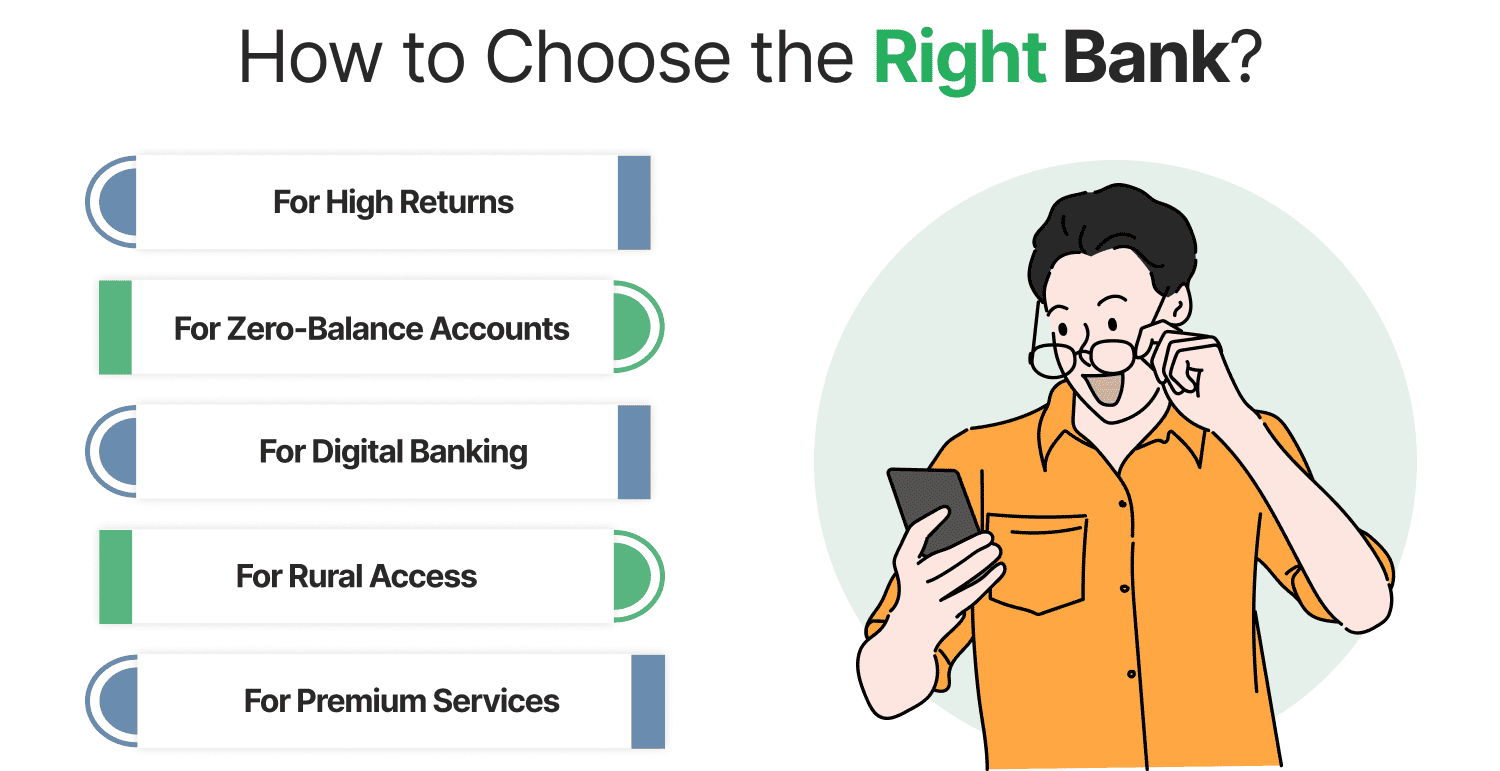

How to Choose the Right Bank?

- For High Returns : AU Small Finance Bank or RBL Bank are ideal for balances above ₹1 lakh, offering up to 7.25%-7.50% p.a.

- For Zero-Balance Accounts : SBI, AU Small Finance Bank , or Federal Bank (NiyoX) suit those avoiding minimum balance penalties.

- For Digital Banking : ICICI (iMobile Pay), Kotak (811 Edge), or IDFC FIRST (zero-fee transactions) are top choices.

- For Rural Access : SBI’s extensive network ensures unparalleled reach.

- For Premium Services : HDFC, Axis, and Yes Bank offer rewards, cashback, and lifestyle benefits.

Conclusion

Selecting the best savings account in India in 2025 depends on your financial priorities. Private banks like HDFC, ICICI, and Kotak excel in digital banking and premium services, while SBI offers unmatched accessibility and reliability. Small finance banks like AU provide high interest rates for savers. Compare interest rates, minimum balance requirements, and additional features to find the account that aligns with your goals. Always verify current rates and terms directly with the bank, as they may change, and ensure your deposits are protected by DICGC up to ₹5 lakh for peace of mind.

Frequently Asked Questions (FAQs)