Top 10 Banks in India

Last Updated : June 16, 2025, 4:13 p.m.

In India’s dynamic financial landscape, choosing the right bank is crucial for secure and efficient financial management. With the growth of digital banking and initiatives like the Pradhan Mantri Jan Dhan Yojana, almost every Indian has access to banking services. This article explores the top 10 banks in India for 2025, focusing on their services, market presence, and customer-centric offerings. Whether you’re looking for a savings account, personal loan, or digital banking solutions, this guide, optimized for banking in India, will help you make an informed decision. For more details on banking products, visit Types of Bank Accounts .

1. HDFC Bank

HDFC Bank leads as India’s largest private sector bank. Known for its robust digital banking platforms like HDFC NetBanking and PayZapp it offers a range of products, including personal loans, home loans, and credit cards. With over 8,000 branches and 20,000 ATMs, HDFC ensures accessibility and convenience. Its savings accounts offer competitive interest rates, and its customer service is top-notch.

2. ICICI Bank

ICICI Bank, the second-largest private bank, excels in online banking and NRI services. With a market cap of ₹8.63L crore, it provides NRE/NRO savings accounts, personal loans, and demat services.

3. State Bank of India (SBI)

SBI, India’s largest public sector bank. With over 22,000 branches, it dominates in reach and trust. SBI offers home loans , vehicle loans, and savings accounts with attractive rates. Its YONO SBI app integrates banking, investments, and shopping, making it a leader in digital banking in India.

4. Axis Bank

Axis Bank is known for its innovative digital banking solutions. It provides personal loans and credit cards with reward points. Axis Mobile App ensures seamless transactions, and its savings accounts cater to diverse customer needs. The bank’s focus on online banking makes it a top choice.

5. Kotak Mahindra Bank

Kotak Mahindra Bank holds the title of the best-performing bank in 2024. It has 811 digital savings accounts and WhatsApp banking. It requires no minimum balance, appealing to young customers. Kotak’s personal loans and credit cards are popular for their flexibility.

6. Bank of Baroda

Bank of Baroda (BOB) is a leading public sector bank offering personal loans up to ₹10 lakh in metro cities and vehicle loans up to ₹100 lakh. Its BOB World app enhances digital banking with features like UPI and bill payments. BOB’s home loan schemes, such as Baroda Home Loan Advantage, are customer favourites.

7. Punjab National Bank (PNB)

PNB, a major public sector bank, offers savings accounts , home loans, and personal loans with competitive rates. Its PNB One app supports digital banking services, including UPI and mobile banking. PNB’s extensive branch network ensures accessibility across urban and rural areas.

8. IndusInd Bank

IndusInd Bank is recognized for its premium banking services, including savings accounts with high interest rates and personal loans with quick disbursal. Its IndusMobile app provides a seamless online banking experience. The bank’s focus on customer satisfaction makes it a top contender.

9. IDBI Bank

IDBI Bank, now a private sector entity, offers innovative products like savings accounts and home loans. Its Go Mobile+ app supports digital banking, making transactions hassle-free. IDBI’s competitive personal loan rates attract customers seeking quick funds.

10. IDFC First Bank

IDFC First Bank, a recent addition to the elite list, offers savings accounts with up to 7% interest and personal loans with flexible repayment options. Its IDFC FIRST Mobile app is user-friendly, supporting digital banking services like UPI and bill payments.

Top 10 Private and Government Banks

| Criteria | Top 10 Private Banks | Top Government (Public Sector) Banks |

|---|---|---|

Examples | 1. HDFC Bank 2. ICICI Bank 3. Kotak Mahindra Bank 4. Axis Bank 5. IndusInd Bank 6. Yes Bank 7. Federal Bank 8. IDFC FIRST Bank 9. AU Small Finance Bank 10. RBL Bank | 1. State Bank of India (SBI) 2. Bank of Baroda 3. Punjab National Bank 4. Union Bank of India 5. Bank of India 6. Canara Bank 7. Indian Bank 8. Indian Overseas Bank 9. Central Bank of India 10. Bank of Maharashtra |

Interest Rates (p.a.) | 3.00% - 8.00% (e.g., AU Small Finance: 3.00%-7.25%, RBL: 3.50%-7.50%, HDFC: 3.00%-3.50%) | 2.70% - 4.00% (e.g., SBI: 2.70%-3.00%, Union Bank: 2.75%-4.00%, Bank of India: 2.75%-2.90%) |

Minimum Balance (INR) | Varies: Nil (e.g., AU Small Finance, Federal NiyoX) to ₹50,000 (e.g., Kotak high-end accounts); Urban/Metro often ₹10,000-₹12,000 (e.g., HDFC, Axis) | Often Nil (e.g., SBI, Union Bank without cheque book) or low (e.g., Union Bank: ₹100-₹1,000, Bank of India: ₹500-₹10,000) |

Branch/ATM Network | Large but smaller than public banks: HDFC (9,092 branches, 20,993 ATMs), ICICI (6,613 branches, 16,120 ATMs); small finance banks have fewer branches | Extensive: SBI (22,500+ branches, 60,000+ ATMs), Bank of Baroda (8,000+ branches); strong rural reach |

Digital Banking | Advanced: ICICI (iMobile Pay), Kotak (811 Edge), IDFC FIRST (zero-fee transactions), Yes Bank (WhatsApp banking); highly user-friendly apps | Improving: SBI (YONO), Canara Bank (CANDI app); less seamless than private banks, varies by bank |

Customer Service | High ratings: HDFC, Axis, Kotak excel in urban areas; AU and IDFC FIRST focus on personalized service | Variable: SBI strong in rural areas, urban service inconsistent; Bank of Baroda, Indian Bank improving but slower |

Additional Features | Cashback (Axis: 15% on Amazon), zero forex debit cards (RBL), monthly interest credits (IDFC FIRST), lifestyle perks (IndusInd), tailored accounts (ICICI women/seniors) | Zero-balance accounts (SBI), financial inclusion focus, government-backed schemes, rural-focused accounts (e.g., Bank of India Mahila account) |

Financial Stability | Strong: HDFC (₹14.8 lakh crore market cap), ICICI (₹8.73 lakh crore); RBI-regulated, deposits insured up to ₹5 lakh by DICGC | Very high: Government-backed, SBI largest public bank; deposits insured up to ₹5 lakh by DICGC |

Account Opening Process | Often fully digital: Kotak 811, IDFC FIRST, Yes Bank via e-KYC; quick and convenient | Mixed: SBI (YONO digital), others may require branch visits; slower for some accounts |

Fees and Charges | Higher penalties for non-maintenance (e.g., HDFC ₹600/quarter in urban areas); some offer zero-fee transactions (IDFC FIRST) | Lower or no penalties (e.g., SBI no minimum balance penalty); minimal charges for digital transactions |

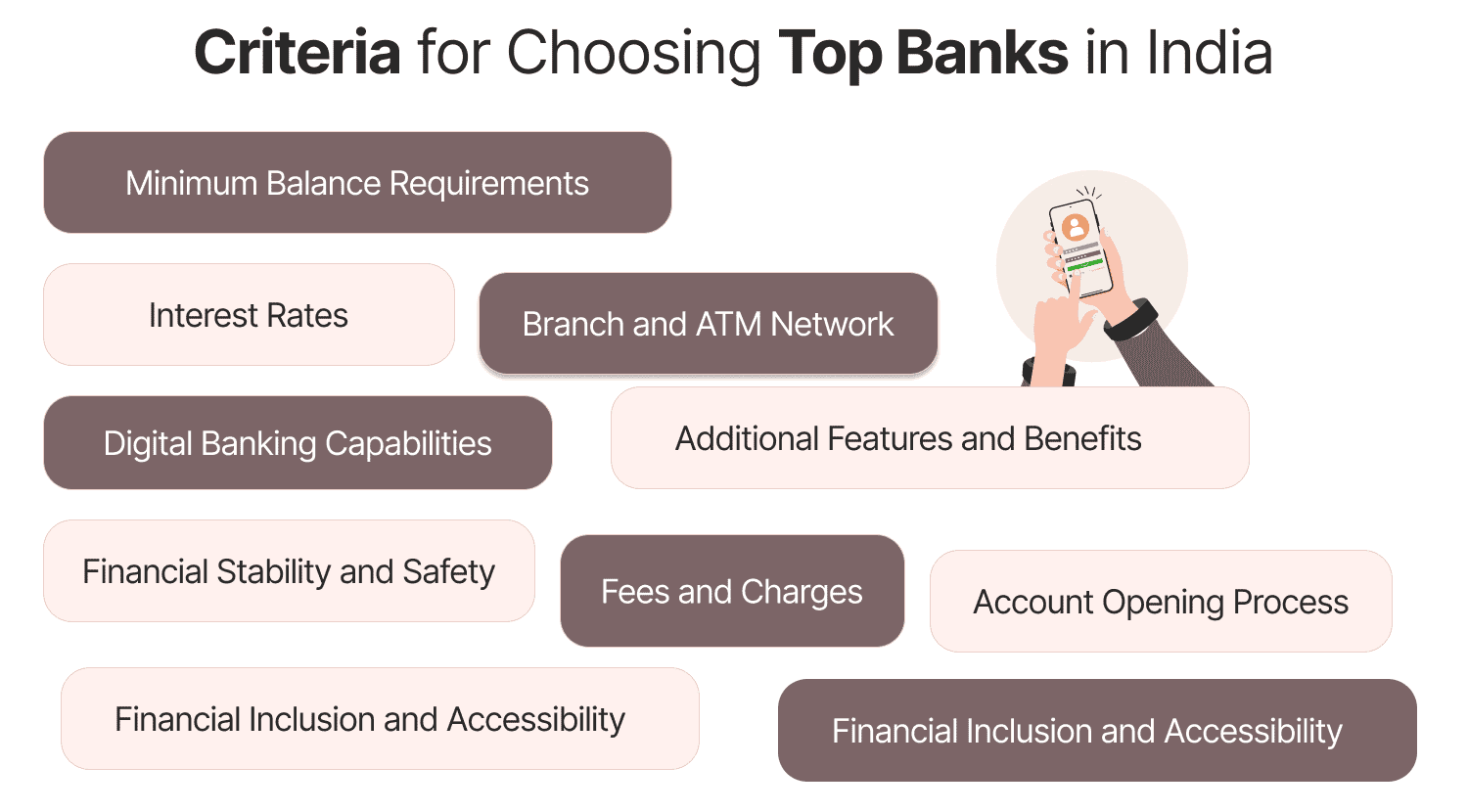

Criteria for Choosing Top Banks in India

Choosing the best bank in India for a savings account in 2025 requires evaluating several key criteria to ensure it aligns with your financial needs and preferences. Below are the primary factors to consider, based on insights from reliable sources and industry trends:

- Interest Rates :

- Importance : Higher interest rates maximize returns on savings.

- Details : Rates range from 2.70% (e.g., SBI) to 8.00% p.a. (e.g., ESAF Small Finance Bank). Small finance banks often offer higher rates (7.00%-8.00%) for larger balances, while larger banks provide 3.00%-4.00%.

- Consideration : Check balance slabs, as rates increase with higher deposits (e.g., IDFC FIRST Bank offers up to 7.00% for balances above ₹1 lakh).

- Minimum Balance Requirements :

- Importance : Avoid penalties by maintaining the required balance.

- Details : Varies by bank and location—zero balance at SBI and AU Small Finance Bank, while HDFC requires ₹10,000 in urban/metro areas. Small finance banks like Equitas may require ₹2,500 (assumed).

- Consideration : Choose zero-balance accounts if maintaining a minimum balance is challenging, especially for rural users.

- Branch and ATM Network :

- Importance : Ensures accessibility for cash withdrawals and in-person services.

- Details : SBI has the largest network (22,500+ branches, 60,000+ ATMs), followed by HDFC (9,092 branches, 20,993 ATMs). Small finance banks have fewer branches, focusing on digital services.

- Consideration : Opt for banks with extensive networks if you prefer physical banking, especially in rural areas.

- Digital Banking Capabilities :

- Importance : Facilitates seamless online transactions and account management.

- Details : Banks like ICICI (iMobile Pay), SBI (YONO), and Kotak (811 Edge) offer advanced apps for transfers, bill payments, and investments. IDFC FIRST provides zero-fee digital transactions.

- Consideration : Prioritize banks with user-friendly apps and features like WhatsApp banking or UPI integration for tech-savvy users.

- Customer Service :

- Importance : Ensures prompt resolution of queries and issues.

- Details : Private banks like HDFC and Axis are rated highly for service (e.g., quick response times), while public sector banks like SBI may vary by branch. Reviews on platforms like MouthShut highlight service quality.

- Consideration : Research customer reviews and complaint resolution rates to gauge reliability.

- Additional Features and Benefits :

- Importance : Enhances the value of the savings account.

- Details : Includes free debit cards (e.g., RBL’s zero forex markup), discounts (e.g., AU’s 25% off Swiggy), monthly interest credits (IDFC FIRST), or specialized accounts (e.g., ICICI’s women/senior accounts).

- Consideration : Look for perks like reward points, cashback, or insurance benefits that align with your lifestyle.

- Financial Stability and Safety :

- Importance : Ensures your deposits are secure.

- Details : Deposits up to ₹5 lakh are insured by DICGC across all banks. Large banks like HDFC (market cap ₹14.8 lakh crore) and SBI are highly stable, while small finance banks are regulated by RBI.

- Consideration : Choose RBI-regulated banks with strong financials, especially for large savings.

- Account Opening Process :

- Importance : Simplifies onboarding, especially for digital accounts.

- Details : Banks like Kotak (811 Digital) and Yes Bank offer instant online account opening via e-KYC. Public sector banks may require branch visits for some accounts.

- Consideration : Opt for banks with fully digital onboarding if convenience is a priority.

- Fees and Charges :

- Importance : Minimizes costs associated with banking.

- Details : Some banks (e.g., IDFC FIRST) offer zero fees for NEFT/RTGS/IMPS, while others charge for non-maintenance of minimum balance (e.g., ₹600/quarter at HDFC in urban areas).

- Consideration : Compare charges for ATM withdrawals, digital transactions, and penalties to avoid hidden costs.

- Financial Inclusion and Accessibility :

- Importance : Supports underserved segments and rural customers.

- Details : SBI and small finance banks like ESAF focus on rural outreach and zero-balance accounts. Public sector banks offer accounts tailored for low-income groups.

- Consideration : Choose banks with inclusive offerings if you’re in a rural area or prefer socially responsible banking.

- Interest Rates :

- Importance : Higher interest rates maximize returns on savings.

- Details : Rates range from 2.70% (e.g., SBI) to 8.00% p.a. (e.g., ESAF Small Finance Bank). Small finance banks often offer higher rates (7.00%-8.00%) for larger balances, while larger banks provide 3.00%-4.00%.

- Consideration : Check balance slabs, as rates increase with higher deposits (e.g., IDFC FIRST Bank offers up to 7.00% for balances above ₹1 lakh).

- Minimum Balance Requirements :

- Importance : Avoid penalties by maintaining the required balance.

- Details : Varies by bank and location—zero balance at SBI and AU Small Finance Bank, while HDFC requires ₹10,000 in urban/metro areas. Small finance banks like Equitas may require ₹2,500 (assumed).

- Consideration : Choose zero-balance accounts if maintaining a minimum balance is challenging, especially for rural users.

- Branch and ATM Network :

- Importance : Ensures accessibility for cash withdrawals and in-person services.

- Details : SBI has the largest network (22,500+ branches, 60,000+ ATMs), followed by HDFC (9,092 branches, 20,993 ATMs). Small finance banks have fewer branches, focusing on digital services.

- Consideration : Opt for banks with extensive networks if you prefer physical banking, especially in rural areas.

- Digital Banking Capabilities :

- Importance : Facilitates seamless online transactions and account management.

- Details : Banks like ICICI (iMobile Pay), SBI (YONO), and Kotak (811 Edge) offer advanced apps for transfers, bill payments, and investments. IDFC FIRST provides zero-fee digital transactions.

- Consideration : Prioritize banks with user-friendly apps and features like WhatsApp banking or UPI integration for tech-savvy users.

- Customer Service :

- Importance : Ensures prompt resolution of queries and issues.

- Details : Private banks like HDFC and Axis are rated highly for service (e.g., quick response times), while public sector banks like SBI may vary by branch. Reviews on platforms like MouthShut highlight service quality.

- Consideration : Research customer reviews and complaint resolution rates to gauge reliability.

- Additional Features and Benefits :

- Importance : Enhances the value of the savings account.

- Details : Includes free debit cards (e.g., RBL’s zero forex markup), discounts (e.g., AU’s 25% off Swiggy), monthly interest credits (IDFC FIRST), or specialized accounts (e.g., ICICI’s women/senior accounts).

- Consideration : Look for perks like reward points, cashback, or insurance benefits that align with your lifestyle.

- Financial Stability and Safety :

- Importance : Ensures your deposits are secure.

- Details : Deposits up to ₹5 lakh are insured by DICGC across all banks. Large banks like HDFC (market cap ₹14.8 lakh crore) and SBI are highly stable, while small finance banks are regulated by RBI.

- Consideration : Choose RBI-regulated banks with strong financials, especially for large savings.

- Account Opening Process :

- Importance : Simplifies onboarding, especially for digital accounts.

- Details : Banks like Kotak (811 Digital) and Yes Bank offer instant online account opening via e-KYC. Public sector banks may require branch visits for some accounts.

- Consideration : Opt for banks with fully digital onboarding if convenience is a priority.

- Fees and Charges :

- Importance : Minimizes costs associated with banking.

- Details : Some banks (e.g., IDFC FIRST) offer zero fees for NEFT/RTGS/IMPS, while others charge for non-maintenance of minimum balance (e.g., ₹600/quarter at HDFC in urban areas).

- Consideration : Compare charges for ATM withdrawals, digital transactions, and penalties to avoid hidden costs.

- Financial Inclusion and Accessibility :

- Importance : Supports underserved segments and rural customers.

- Details : SBI and small finance banks like ESAF focus on rural outreach and zero-balance accounts. Public sector banks offer accounts tailored for low-income groups.

- Consideration : Choose banks with inclusive offerings if you’re in a rural area or prefer socially responsible banking.

Conclusion

Selecting the right bank in 2025 depends on your needs—be it savings accounts, personal loans, or digital banking. The top 10 banks in India, including HDFC, ICICI, and SBI, offer trusted services backed by technology and accessibility. Evaluate their offerings to find the best fit for your financial goals.

Frequently Asked Questions (FAQs)