How Much Credit Score is Required to Get a Personal Loan/Home loan?

Last Updated : Dec. 31, 2024, 4:14 p.m.

When you apply for a personal loan or home loan, lenders will look at your credit score to approve your loan application. This score is a number between 300 to 900, and it summarizes your credit history. Credit score in India is provided by 4 credit bureaus namely TransUnion CIBIL, Equifax, Experian, and CRIF HighMark. TransUnion CIBIL is India’s leading credit information company. It provides an accurate and trusted credit score which is called the CIBIL score. Let us now read and understand how much CIBIL score is needed to get a personal loan or home loan.

What CIBIL Score is Required to Get a Personal Loan or Home Loan?

The minimum CIBIL score required to get a personal loan or home loan varies across banks and lenders. However, an ideal score is one between 720 to 750. For a score in this range, lenders will approve your loan application instantly and give you a favourable interest rate. Some lenders may even give you a loan for a CIBIL score of 600. Let us now understand the range of CIBIL scores and what they mean

Do you want to check your CIBIL score? If so, do a free CIBIL score check at Wishfin here .

CIBIL score range | Credit Rating | Meaning |

|---|---|---|

NA/NH | No credit history | You do not have a valid CIBIL history or a CIBIL score under your name. |

Below 600 | Immediate action is required | Chances of approval are very low. |

600 to 649 | Doubtful | You will be charged high interest rates on loans and credit cards. Approval can be really hard. |

650 to 699 | Fair | Options for lenders are limited but approval of credit is possible |

700 to 749 | Good | Can become eligible for better interest rates |

750 to 900 | Excellent | Eligible for low interest rates and higher chances of approval. |

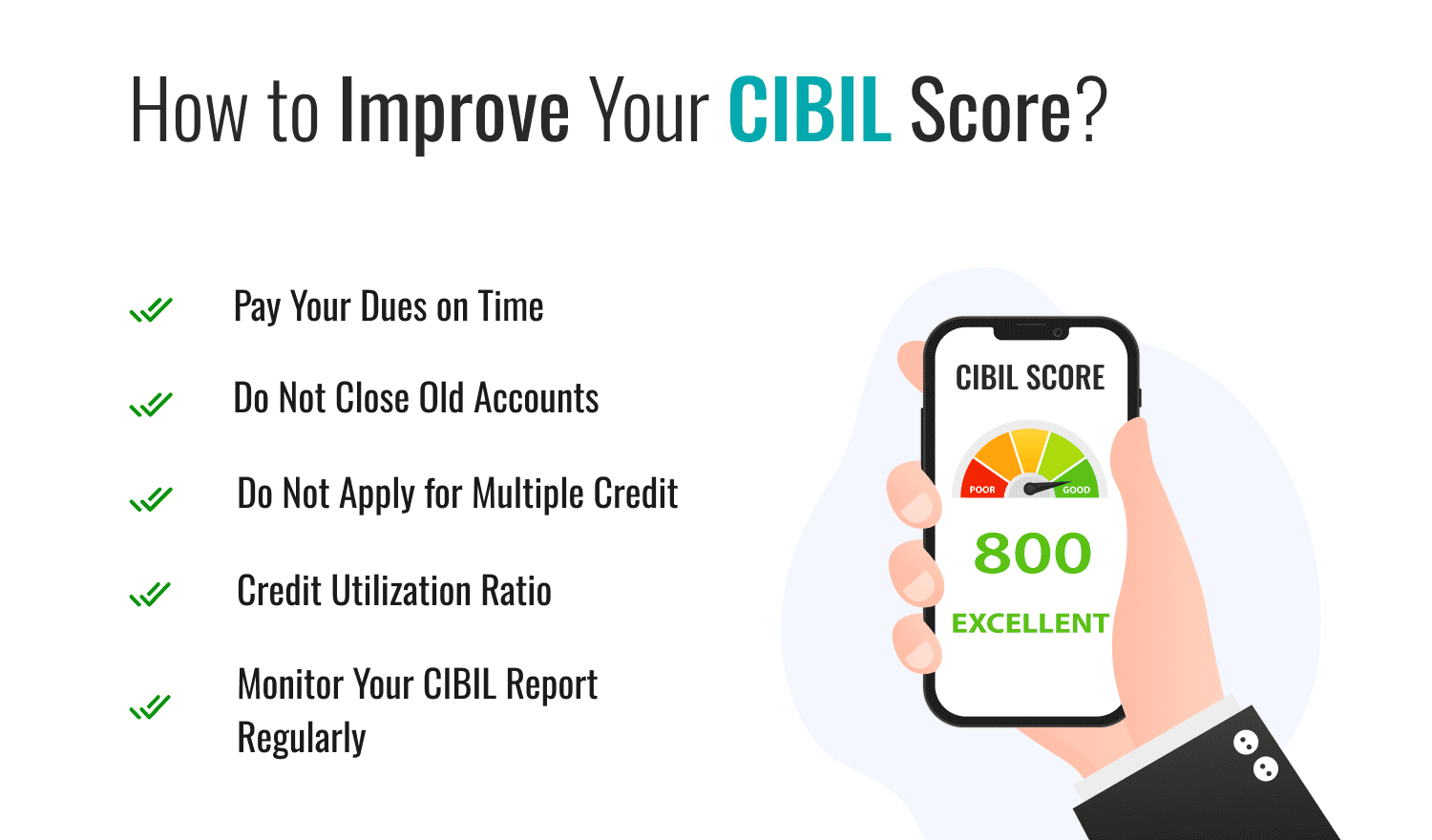

How to Improve Your CIBIL Score?

Pay Your Dues on Time: Timely payment of loan EMIs and credit card bills is important to maintain a good CIBIL score and improve it.

Do Not Close Old Accounts: Your CIBIL score depends on the length of your CIBIL history. Hence do not close your oldest active account.

Do Not Apply for Multiple Credit: Do not keep applying for credit as you may be perceived as credit hungry. When you have several credit applications, you will be seen as having a financial crisis. Hence, apply for credit only when required.

Monitor your CIBIL Report Regularly: Monitoring your CIBIL report regularly is a good practice. In this way, you can instantly clear errors which bring down your CIBIL score by disputing them with CIBIL.

Credit Utilization Ratio: The credit utilization ratio is the ratio of the credit utilized to the overall credit limit available to you. Experts recommend a CUR must be within 30%. To decrease the CUR, you can reduce your dependency on credit or get your credit limit increased. However, even if your CUR is high and you make your payments on time, CIBIL or any other credit bureau will not penalize you.

How Much Credit Score Do You Need for Personal Loan Approval?

As personal loans are available without any security or collateral, there’s a greater degree of credit risk on the part of lenders. Seeing the high credit risk on the cards, they like to approve personal loan applications of individuals having a credit score of 750 and beyond. Having said that, you can get the approval even with a score of 700-750.

How Much Credit Score Do You Need for Home Loan Approval?

Home loans are secured by an equitable mortgage of the property you wish to buy with the same. As the lender keeps the original property documents till the time the loan is on, the degree of credit risk is far lesser than a personal loan. And this is the reason lenders can relax their credit score norms on the same. So even if your credit score is 650 or below, you can get a home loan .

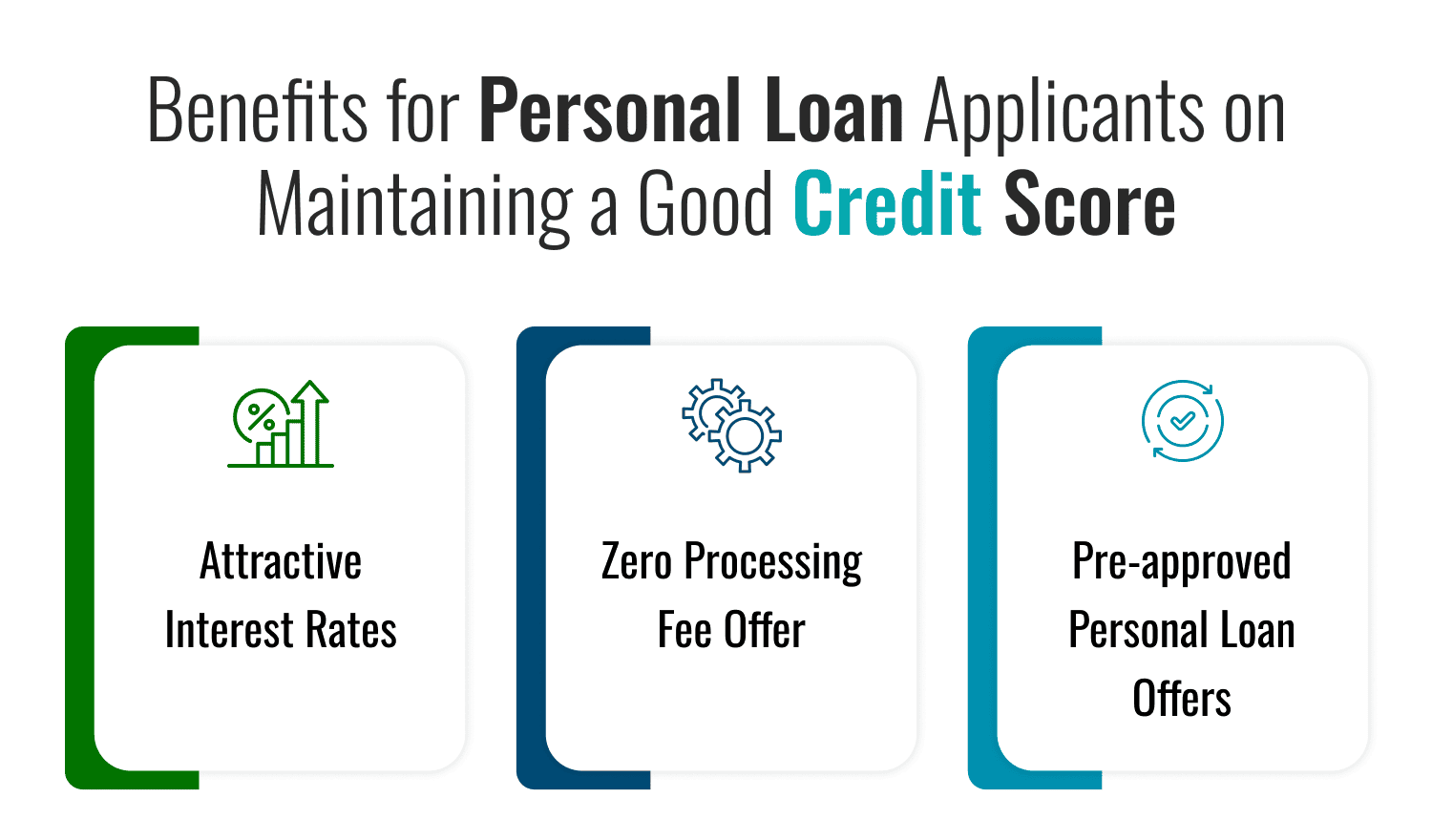

Benefits for Personal Loan Applicants on Maintaining a Good Credit Score

There are numerous benefits available to borrowers applying for a personal loan with a good credit score. Check them below.

Attractive Interest Rates – Personal loan interest rates are usually on the higher side at 11%-20% per annum on average. Having a good credit score of 750 and beyond can prompt lenders to offer you an attractive interest rate deal. The deal will maximize your savings with reduced EMI obligations.

Zero Processing Fee Offer – Processing fee is a concept that many don’t understand fully. Yes, it’s a one-time non-refundable fee that you pay to the lender. You must have read it a number of times. But have you gone on to check how it works out? If not, let us tell you that the fee lowers the net loan disbursement. But the rate of interest will apply to the application amount.

So, if you apply for a personal loan worth INR 5 lakh and the processing fee is INR 8,000, the net loan disbursement will be INR 4,92,000. But the interest rate will apply to INR 5 Lakh. With an excellent credit score of 750 and above, lenders can also give you a zero processing fee offer, making both gross and net loan disbursement the same.

Pre-approved Personal Loan Offers – Your solid repayment track of credit card or any other credits resulting from a good credit score can help you get pre-approved personal loan offers.

Benefits for Home Loan Borrowers Maintaining a Good Credit Score

Attractive Interest Rate Deals – Although credit scores are not considered that important in home loans as they are in personal loans, having a good one will make lenders feel that you are the candidate for a long run. To have you for long, the rate can ease considerably. Home loan rates now mirror the external benchmark of Repo Rate, the rate at which the Reserve Bank of India (RBI) lends to commercial banks for their short-term obligations. The interest rate is arrived after adding spread over the benchmark. That spread usually takes into account the credit record of an individual. So, if the credit score is good, don’t be surprised to get a lower spread. This will eventually reduce the lending rate.

Higher Loan Eligibility – Loan eligibility is determined on the basis of your age, income, the property value, and your repayment capacity. Having a good credit score will give lenders a numerical representation of high creditworthiness. This will only heighten the possibility of buying a home that costs very high.

But, Is the Credit Score Enough to Get a Personal Loan or Home Loan?

When you apply for a loan, the lender pulls out your credit report, which besides telling your credit score, also highlights your repayment behaviour, such as the schedule of payment dates, the extent of credit limit utilization, etc. Your credit score may be good, but some dark spots in your credit report can make lenders wary of disbursing any of the two loans.

How Can You Check Your Credit Score & Credit Report?

Credit bureaus such as CIBIL and Experian provide credit scores and credit reports of individuals and businesses. You can check the same on the official website of these bureaus. If you don’t have an account there, you need to first create it by mentioning your personal and credit details. All these details will be checked thoroughly before you’re allowed to create an account. Free credit score checks are available only once a year. If you do more than once a year, charges will be levied. However, you can do so as many times as you can at Wishfin, a premier fintech portal having got the right to distribute credit scores and credit reports generated by CIBIL and Experian, for free.

Frequently Asked Questions (FAQs)