Credit Inquiries and How They Impact Your Credit Prospects?

Last Updated : Jan. 14, 2025, 6:30 p.m.

Credit inquiries are requests made for credit reports from credit bureaus. Credit inquiries can be made for various reasons by individuals, employers, lenders, or businesses. There are two types of credit inquiries - A hard inquiry and soft inquiry. Let us now understand what each of them is and what impact they have on your credit prospects..

Hard Credit Inquiry

A hard credit inquiry is a credit pull done by a financial institution in order to determine your current financial situation. When you apply for credit, lenders check your credit report to know your payment history, number of outstanding debts, credit history, etc. Hard inquiries can also be triggered when you apply for jobs that require credit checks or when you rent out an apartment.

Impact of a Hard Inquiry on Your Credit Score

- Hard inquiries damage your credit score, and this will differ according to your overall credit history. If you have a strong credit history, a single hard inquiry may only lead to a small decrease in credit score. However, if your credit history is average, then a hard inquiry can hurt your credit score and your credit prospects.

- When lenders see a hard inquiry on your credit report, they will understand that you have recently applied for credit with another financial institution. While it may be indicative of the need for more debt, lenders will also understand that potential applicants often research for the best loans or credit card offers. So, a few hard inquiries will not damage your credit score if you have a robust credit history. However, if your credit history is just average, then lenders may worry about the hard inquiries on your credit report.

Soft Inquiries

A soft inquiry occurs when you check your own credit report. It could also be that a firm has limited information about you to make a promotional offer. So, they may check your credit report for that. A soft inquiry may appear on your credit report, and only you will have access to them. A soft inquiry will not hurt your credit score. A soft inquiry is a credit pull done only for informational purposes, and it will not impact your credit score or credit prospects.

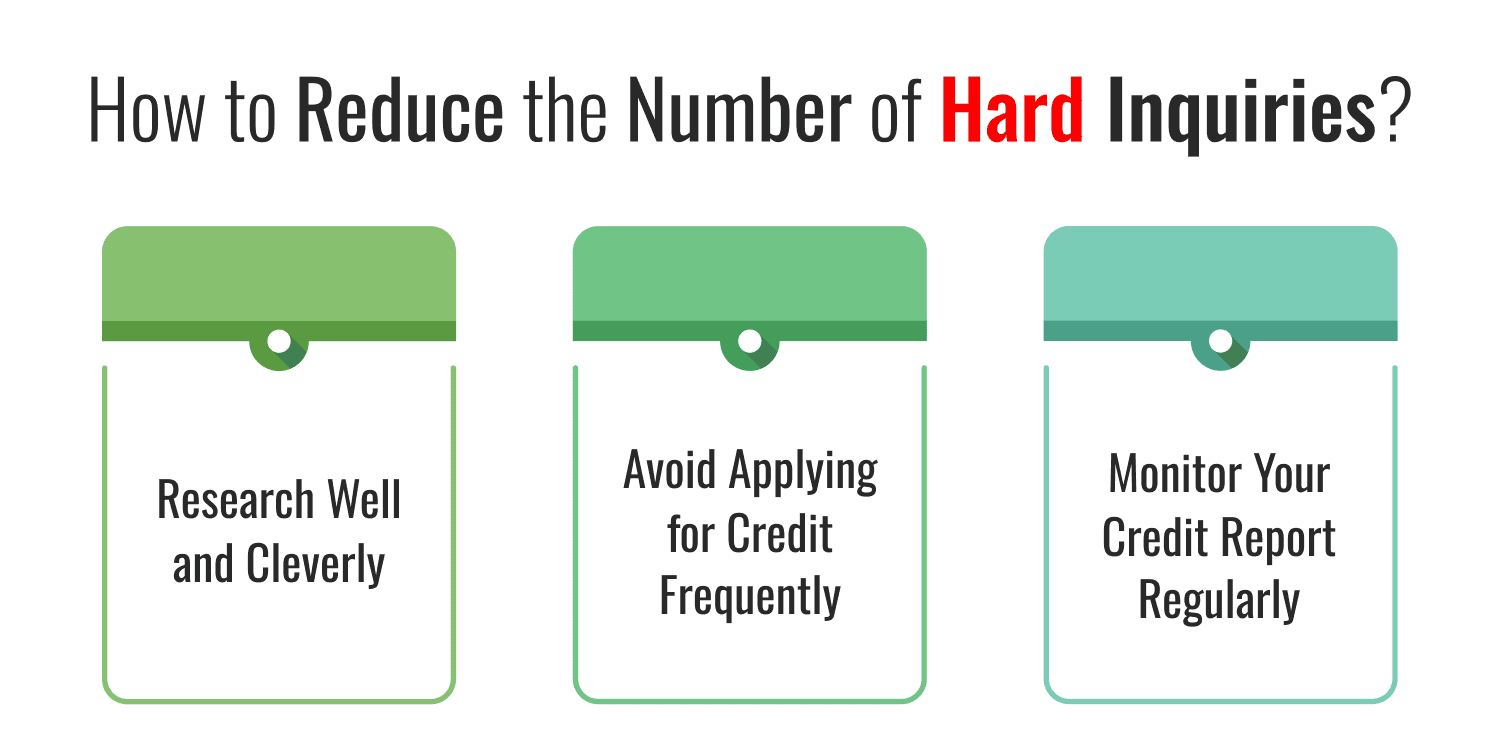

How to Reduce the Number of Hard Inquiries?

Here are some tips to reduce the number of hard inquiries on your credit report.

- Research Well and Cleverly: Before applying for loans or credit cards. Be selective about the credit cards or loans that you want to take. Compare them and finally choose the one which aligns with your financial needs and also has higher approval chances.

- Avoid Applying for Credit Frequently: Do not submit multiple credit applications in a short period of time. Take some time and evaluate your financial status. Then, decide whether you need additional credit before applying. Applying for multiple credit may trigger many hard inquiries.

- Monitor Your Credit Report Regularly: Monitor your credit report regularly. Stay informed about the hard inquiries on your credit report and ensure they are accurate. If you find any discrepancies, ensure to inform the credit card issuer or the credit bureaus.

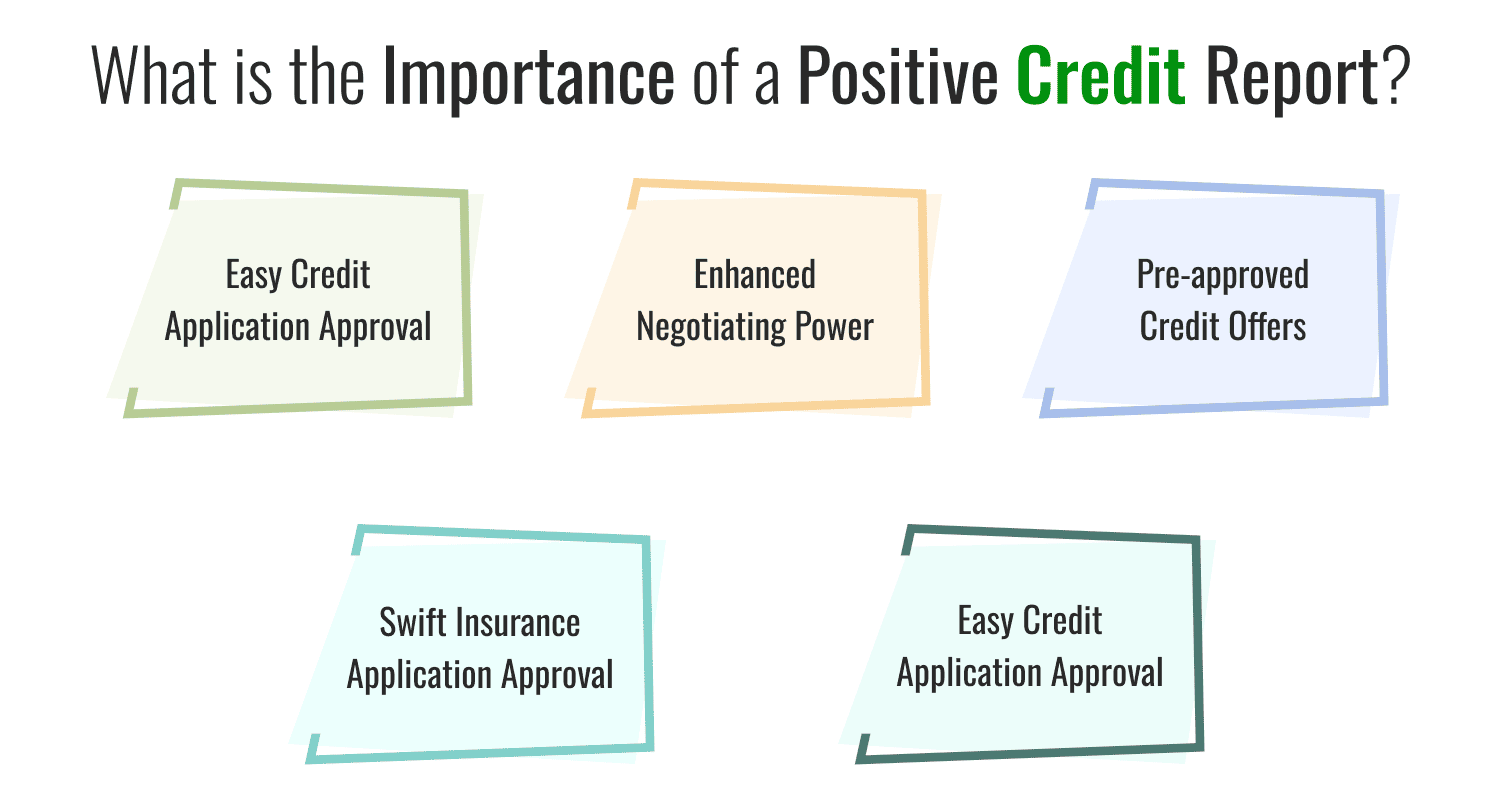

What is the Importance of a Positive Credit Report?

A positive credit report indicates that you are highly creditworthy to various entities like financial institutions, employers, landlords, etc. A credit report contains personal details, employment details, credit account details, loan application history, repayment history details, public records, and credit scores. Here are some benefits of maintaining a good credit report.

- Easy Credit Application Approval: Your credit application gets approved easily without any hassles. All financial institutions will be ready to give you credit. You can compare between the options and choose one that suits your financial needs.

- Enhanced Negotiating Power: You will have the power to negotiate with lenders for preferential interest rates, higher loan amounts, higher credit limits, and better loan terms.

- Preapproved Credit Offers: You will get pre-approved loan offers with higher amounts and best interest rates or pre-approved credit card offers with higher credit limits and bonus perks.

- Swift Insurance Application Approval: Insurance companies will also evaluate your credit history and credit score to measure your capacity to pay the premium on time. Hence a positive credit report increases your chances of getting your insurance application approved.

- Increased Chances of Employment: Although not practiced globally, some employers may check the credit reports of employees during background verifications. Defaulting frequently may indicate irresponsibility and financial instability. A good credit score on the other hand increases your prospects of employability.

Frequently Asked Questions (FAQs)