Understanding Your Credit Report: A Step-by-Step Guide

Last Updated : June 2, 2025, 4:12 p.m.

Your credit report is a snapshot of your financial health, influencing your ability to secure loans, credit cards, and favorable interest rates. For many in India, navigating a credit report can seem daunting, but it’s a crucial step toward financial empowerment. This step-by-step guide from Wishfin will help you understand your credit report, interpret its components, and take action to improve your creditworthiness.

What Is a Credit Report?

A credit report is a detailed record of your credit history, compiled by credit bureaus like CIBIL, Experian, Equifax, or CRIF High Mark in India. It includes information about your loans, credit cards, payment history, and inquiries made by lenders. Understanding your credit report is essential for securing financial products like personal loans or home loans .

Why Is Your Credit Report Important?

Your credit report directly impacts your credit score, which lenders use to assess your creditworthiness. A strong credit score (750+ on CIBIL) can lead to better loan terms, lower interest rates, and higher approval chances. Regularly reviewing your credit report helps you spot errors, detect fraud, and maintain a healthy financial profile.

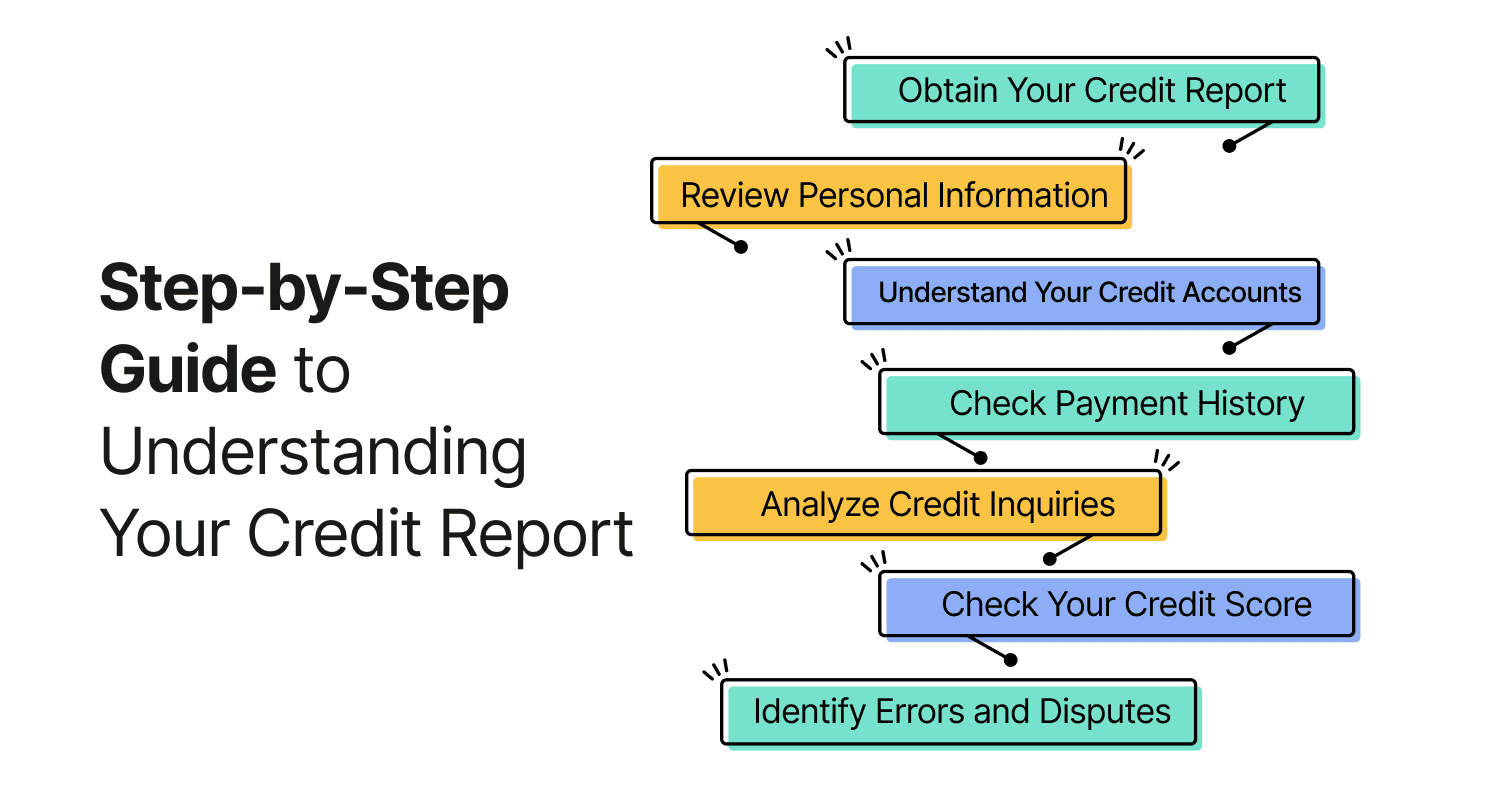

Step-by-Step Guide to Understanding Your Credit Report

Step 1: Obtain Your Credit Report

You can access your credit report from credit bureaus or through platforms like Wishfin, which offers free credit score checks. Visit Wishfin’s free credit score page to get started. By law, you’re entitled to one free credit report annually from each bureau.

Step 2: Review Personal Information

The first section of your credit report contains personal details, including:

- Name, date of birth, and address.

- PAN number, Aadhaar, or other identification details.

- Contact information like phone number and email.

Action: Check for inaccuracies, such as misspelled names or outdated addresses, as these can affect your credit profile. Report errors to the credit bureau for correction.

Step 3: Understand Your Credit Accounts

This section lists all your credit accounts, including:

- Type of account (e.g., home loan, personal loan, credit card ).

- Account status (active, closed, or defaulted).

- Loan amount, outstanding balance, and credit limit.

- Date of account opening and last activity.

Action: Verify that all accounts belong to you. Unfamiliar accounts could indicate identity theft. Ensure loan amounts and statuses are accurate.

Step 4: Check Payment History

Your payment history shows how consistently you’ve paid your EMIs or credit card bills. It’s often represented as:

- “STD” (Standard): Payments made on time.

- “DPD” (Days Past Due): Number of days late on payments (e.g., 30, 60, 90).

- “SMA” (Special Mention Account): Early signs of payment stress.

Action: Late payments or defaults can lower your credit score. Address overdue payments immediately and set up reminders for future EMIs.

Step 5: Analyze Credit Inquiries

This section lists inquiries made by lenders when you apply for credit. There are two types:

- Hard Inquiries: When you apply for a loan or credit card, impacting your score if too frequent.

- Soft Inquiries: When you check your own credit or lenders pre-qualify you, with no impact.

Action: Limit hard inquiries by applying for credit selectively. Multiple inquiries in a short period can signal financial distress.

Step 6: Check Your Credit Score

Your credit score (300-900 in India) is often included in the report. A score above 750 is considered excellent, while below 600 may limit loan approvals.

Action: Use Wishfin’s tools to monitor your score and understand factors affecting it, such as high credit utilization or missed payments.

Step 7: Identify Errors and Disputes

Errors in your credit report, like incorrect balances or unauthorized accounts, can harm your score. Common issues include:

- Incorrect personal details.

- Closed accounts listed as active.

- Duplicate or fraudulent accounts.

Action: File a dispute with the credit bureau online or via mail, providing supporting documents like bank statements or ID proof. Wishfin can guide you through the dispute process.

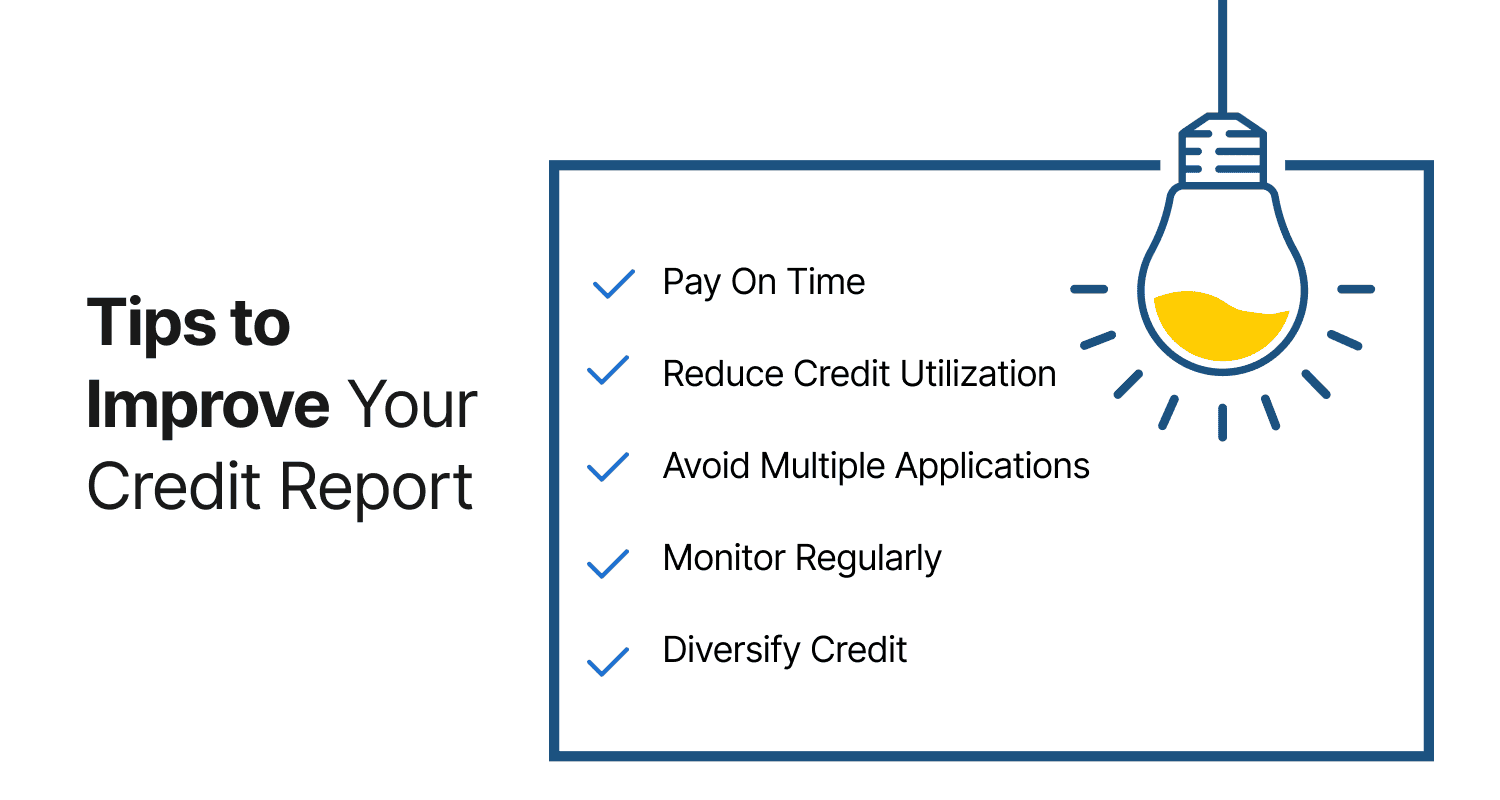

Tips to Improve Your Credit Report

- Pay On Time: Timely EMI and credit card payments boost your score.

- Reduce Credit Utilization: Keep credit card balances below 30% of your limit.

- Avoid Multiple Applications: Space out loan or card applications to minimize hard inquiries.

- Monitor Regularly: Check your credit report quarterly using Wishfin’s free credit score tool .

- Diversify Credit: A mix of secured (e.g., home loans) and unsecured (e.g., personal loans) credit can strengthen your profile.

How Wishfin Can Help?

Wishfin simplifies the process of understanding and managing your credit report. Our platform allows you to check your credit score, compare financial products like personal loans, and access tools to improve your financial health. Start your journey to better credit today with Wishfin’s expert resources.

Conclusion

Understanding your credit report is the first step toward financial independence. By following this step-by-step guide, you can decode your report, spot errors, and take action to improve your credit score. A healthy credit report opens doors to better loan terms and financial opportunities. Leverage Wishfin’s tools and resources to stay on top of your credit health and make informed financial decisions in 2025.

Frequently Asked Questions (FAQs)