Education Loan for Abroad Studies - Everything You Need to Know in 2026

Last Updated : March 16, 2026, 12:13 p.m.

Studying abroad is one of the most powerful investments a student can make in their future. But tuition fees, living expenses, travel, and other costs at foreign universities can easily run into ₹30–₹80 lakh or more. For most Indian families, an education loan is the most practical and strategic way to fund this dream.

In 2026, education loans for abroad studies are more accessible than ever with government schemes, collateral-free options, and tax benefits making them highly attractive. This guide covers everything: eligibility, top banks, interest rates, documents needed, and how to apply.

What is an Education Loan for Abroad Studies?

An education loan for abroad studies (also searched as educaton loan abroad or education lone for foriegn country) is a financial product offered by banks and NBFCs to help Indian students fund their higher education at universities outside India.

These loans cover:

- Tuition fees paid directly to the university

- Living expenses (hostel, food, transportation)

- Books, equipment, and laptops

- Travel expenses (airfare to and from India)

- Health and travel insurance

- Study materials and exam fees

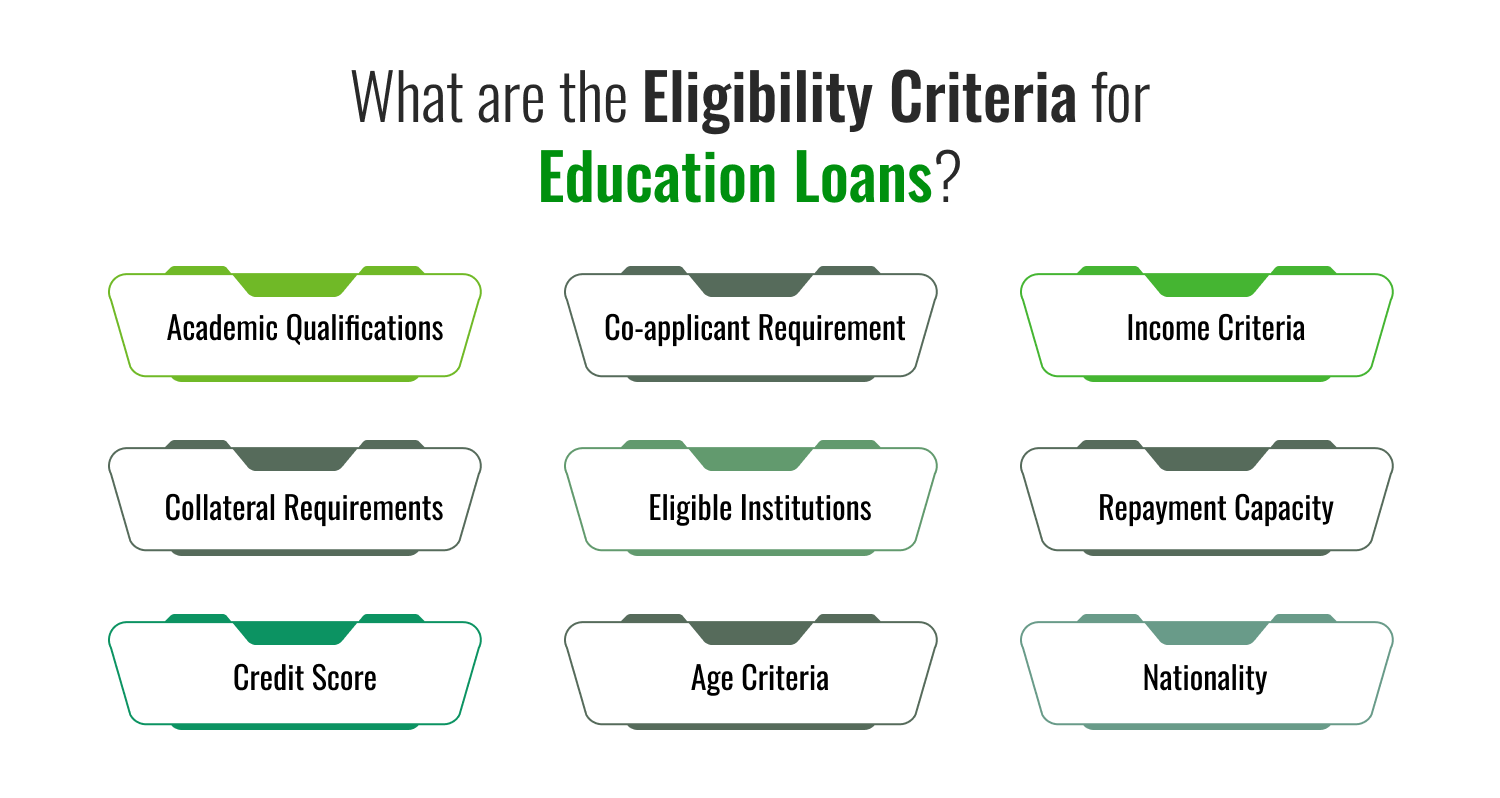

Education Loan Eligibility for Abroad Studies

To be eligible for an education loan for foreign studies, you generally need to meet these criteria:

| Criterion | Requirement |

|---|---|

| Nationality | Indian citizen |

| Age | 18–35 years (varies by bank) |

| Academic qualification | 10+2 / Graduation completed |

| Admission | Confirmed admission letter from a recognized foreign university |

| Course type | UG, PG, PhD, Professional (MBA, MS, MD, etc.) |

| Co-applicant | Parent / Spouse / Guardian (mandatory for most banks) |

| CIBIL Score | 700+ (co-applicant's score matters most) |

Top Banks for Education Loan for Abroad Studies: Interest Rate Comparison 2026

| Bank | Interest Rate (p.a.) | Max Loan Amount | Collateral Required |

|---|---|---|---|

| SBI Global Ed-Vantage | 9.15% – 11.15% | ₹1.5 crore | Above ₹7.5 lakh |

| Bank of Baroda Baroda Scholar | 9.70% – 10.60% | ₹80 lakh | Above ₹7.5 lakh |

| HDFC Credila | 10.50% – 13.50% | ₹1 crore | Flexible |

| Axis Bank | 10.70% – 13.50% | ₹75 lakh | Above ₹7.5 lakh |

| ICICI Bank | 11.25% – 14.00% | ₹1 crore | Flexible |

| Avanse Financial | 11.00% – 14.00% | ₹75 lakh | Flexible |

| InCred | 11.50% – 14.00% | ₹60 lakh | No collateral options |

Note: Interest rates for girl students are typically 0.50% lower at public sector banks.

Education Loan Without Collateral for Abroad Studies

A major concern for many families is not having a property to pledge as collateral. Here is the good news — you can get an education loan without collateral (unsecured) for amounts up to ₹7.5 lakh under the IBA Model Loan Scheme at public banks. For higher amounts, these options exist:

- NBFCs like Avanse, InCred, HDFC Credila — These institutions offer collateral-free education loans up to ₹50–₹75 lakh based on the student's academic profile, university ranking, and course employability.

- Government Guarantee Schemes — The Credit Guarantee Fund Scheme for Education Loans (CGFSEL) allows banks to extend collateral-free loans up to ₹7.5 lakh.

- PM Vidya Lakshmi Portal — A government-backed single window platform where you can apply to multiple banks for education loans simultaneously.

Tax Benefit on Education Loan: Section 80E

This is one of the most underused benefits of an education loan. Under Section 80E of the Income Tax Act , the interest paid on an education loan is fully deductible from your taxable income — with no upper limit .

- Benefit available for up to 8 consecutive years starting from the year you begin repayment

- Applies to loans taken for self, spouse, children, or a student for whom you are a legal guardian

- Applicable to courses pursued in India or abroad

For a student who takes a ₹40 lakh loan at 11% interest, the annual interest in year 1 is approximately ₹4.4 lakh — which is fully tax-deductible, saving ₹1.3–₹1.5 lakh in taxes per year.

Documents Required for Education Loan Abroad

Student Documents:

- KYC - Aadhaar, PAN

- Academic mark sheets (10th, 12th, graduation)

- Confirmed admission/acceptance letter from foreign university

- Fee structure / cost of attendance letter from the university

- Entrance exam scorecards (GRE, GMAT, IELTS, TOEFL)

- Visa (if already received)

Co-applicant / Parent Documents:

- KYC - Aadhaar, PAN

- Income proof - salary slips / ITR (last 2–3 years)

- Bank statements (last 6–12 months)

- Property documents (if pledging collateral)

Repayment: When Do You Start Paying?

Education loans come with a moratorium period - you don't need to start repaying immediately. Repayment typically starts:

- 6–12 months after course completion , OR

- When you get a job (whichever is earlier)

During the moratorium, simple interest continues to accrue. Paying even the simple interest during this period reduces your total loan burden significantly.

Frequently Asked Questions (FAQs)