IDFC First Bank Credit Card Late Payment Charges

Last Updated : June 16, 2025, 5:40 p.m.

Managing your credit cards effectively is crucial for maintaining a healthy financial profile, and timely credit card payments are a key part of this. For IDFC First credit cards, understanding the IDFC First Bank Credit Card Late Payment Charges can help you avoid unnecessary fees and protect your CIBIL score. IDFC First Bank offers a range of lifetime-free credit cards with attractive rewards, low interest rates, and flexible payment options. However, missing IDFC First credit card payments can lead to penalties that impact your finances and creditworthiness. This article dives into the details of IDFC First Bank Credit Card Late Payment Charges, how they are calculated, their impact on your CIBIL score , and tips to ensure timely IDFC First credit card payments.

What Are IDFC First Bank Credit Card Late Payment Charges?

When you miss paying the minimum amount due on your credit card by the due date, IDFC First Bank will levy charges for defaulting on your payments. These are called IDFC First Bank Credit Card Late Payment Charges?They are designed so that you make credit card payments on time (Since you will not want to increase your debt burden by paying these fees). According to IDFC First Bank’s fee schedule, late payment penalties are as follows:

| Outstanding amount | Charges |

|---|---|

Less than Rs. 100 | No charges |

Rs. 101 to Rs. 500 | Rs. 100 |

Rs. 501 to Rs. 5,000 | Rs. 750 |

Rs. 5,001 to Rs. 8000 | Rs. 1200 |

₹8001 to Rs. 10,000 | Rs. 1300 |

More than Rs. 10,000 | Rs. 1300 |

These charges are in furtherance to the interest in the range of 8.5% to 46.2% per annum. This interest is applied to the unpaid balance.

For the IDFC First SWYP Credit Card, the penalties vary and are as follows:

| Outstanding amount | Charges |

|---|---|

Less than Rs. 100 | None |

Rs. 101 to Rs. 500 | Rs. 100 |

Rs. 501 to Rs. 5000 | Rs. 750 |

Rs. 5001 to Rs. 10,000 | Rs. 1500 |

Rs. 10001 to Rs. 20,000 | Rs. 3,000 |

More than Rs. 20,000 | Rs. 3,000 |

How Are IDFC First Bank Credit Card Late Payment Charges Computed?

Late payment charges are calculated as 15% of the total amount due as of the previous statement minus any payments received before the due date with a minimum charge of Rs. 100 and maximum charge of Rs. 1300. IDFC FIRST Bank can alter the charges anytime from time to time with prior notice. So for the most recent charges, check the Schedule of Charges published on the IDFC Bank website.

IDFC First Credit Card Cash Withdrawal Charges

When you use your IDFC First credit card to withdraw cash from an ATM, a cash advance transaction fee is applied. For most IDFC First Bank credit cards , these charges are Rs. 199 per transaction. Exclusions include:

FIRST Private Credit Card: No cash advance fee.

FIRST Digital RuPay Credit Card: Cash advance facility not available.

In addition to the transaction fee, interest is charged on the withdrawn amount from the date of withdrawal until it is fully repaid, with no interest-free period. The interest rate for cash advances matches that for purchases, ranging from 8.5% to 46.2% per annum, depending on your credit profile. This makes cash withdrawals a costly option, so they should be used only in emergencies. For detailed terms, refer to the IDFC First Bank Schedule of Charges.

IDFC First Bank Credit Card Forex Charges

When using your IDFC First credit card for international transactions, you may incur forex (foreign exchange) markup charges. These charges constitute a percentage of the transaction amount and differ across card types. Below are the forex markup charges for important IDFC First Bank credit cards:

| Card Type | Forex Markup Fee |

|---|---|

IDFC FIRST WOW! Credit Card | 0% |

IDFC FIRST Wealth Credit Card | 1.50% |

FIRST Private Credit Card | 0% |

Mayura Credit Card | 0% |

Club Vistara IDFC FIRST Credit Card | 2.99% |

For other IDFC First credit cards, forex markup rates may change, and customers should refer to the IDFC First Bank Schedule of Charges for precise rates. Foreign currency transactions are converted to Indian Rupees (INR) through US Dollars on the settlement date, using rates given by VISA, RuPay, or MasterCard, depending on the network of the card. IDFC First Bank also offers Dynamic Currency Conversion (DCC) at international merchants or ATMs, allowing payments in INR, but this may include fees from the acquiring bank or service provider. Choosing a card like the IDFC FIRST WOW! with zero forex fees can significantly reduce costs for frequent international travelers.

Other IDFC First Bank Credit Card Charges

Beyond late payment and cash withdrawal fees, IDFC First credit cards come with additional charges that cardholders should be aware of. Below is a table summarizing key charges applicable to most cards, though fees may vary by card variant:

| Charge Type | Amount/Details |

|---|---|

Cash Advance Transaction Fee | ₹199 per transaction (For most cards. However it is zero for FIRST Private; N/A for FIRST Digital RuPay) |

Late Payment Charges | 15% of total amount outstanding (min ₹100, max ₹1,300 for most cards; max ₹3,000 for FIRST SWYP) |

Over-limit Charges | 2.5% of the over-limit amount (Minimum Rs. 550; not levied on some cards like FIRST Private) |

Foreign Currency Markup | 1% to 3.50% of transaction value, depending on card variant (e.g., 1% for Select, 3.50% for Mayura) |

Card Replacement Fee | ₹200 for most cards; huger for premium cards (e.g., ₹4,000 for FIRST Private) |

Reward Redemption Fee | ₹99 for every recovery (Not applicable for FIRST Private, Club Vistara) |

Annual Fee | Varies across cards; many are lifetime free (e.g., FIRST Classic: ₹499) |

Note: All fees exclude Goods and Services Tax (GST), 18% at the present, subject to change according to government regulations. For a complete list of charges specific to your card, visit the official website of the bank.

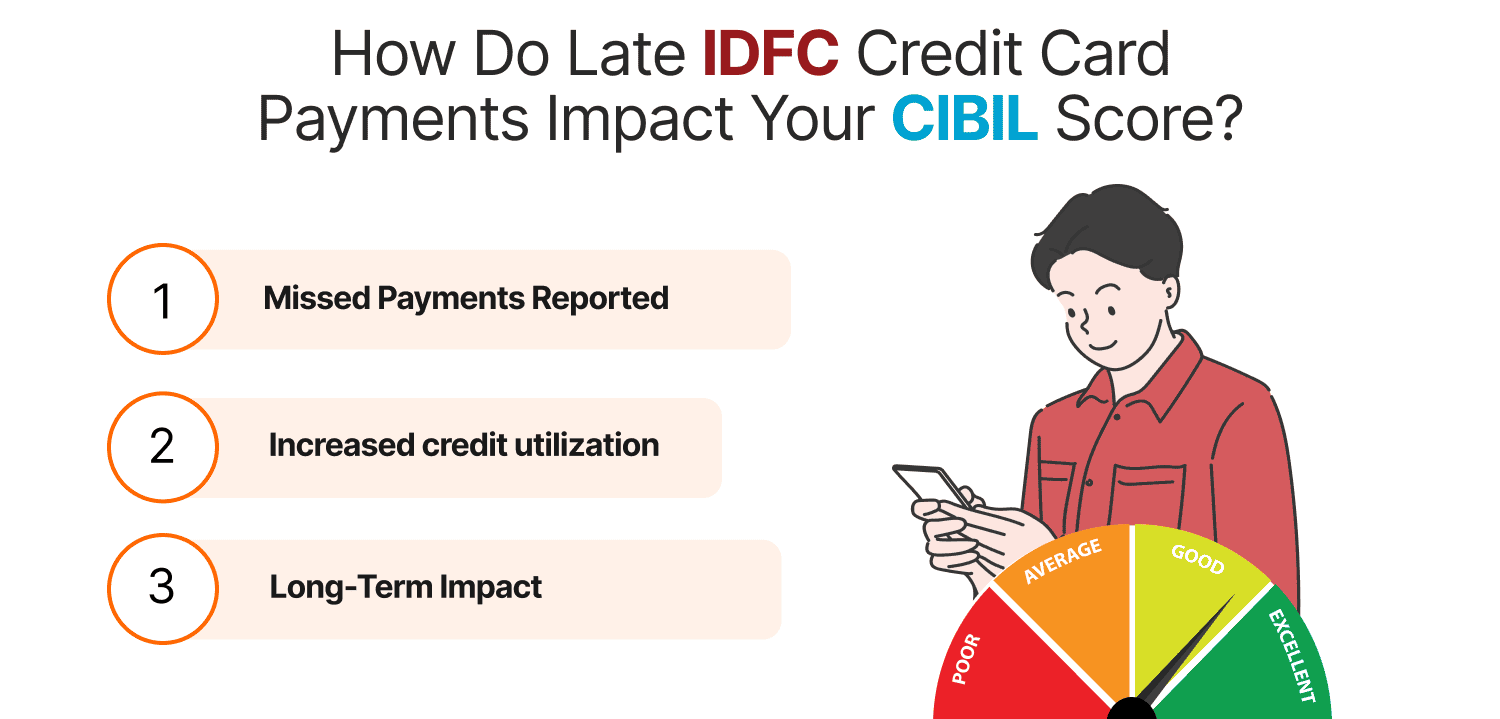

How Do Late IDFC Credit Card Payments Impact Your CIBIL Score?

Your CIBIL score is a three-digit number that lies in the range of 300 to 900. It reflects your creditworthiness. Making delayed IDFC First credit card payments can be highly detrimental to your credit score. Here’s how:

- Missed Payments Reported: IDFC First Bank reports late payments to credit bureaus like CIBIL. Even a single missed payment can lower your CIBIL score by 50–100 points, depending on your credit history

- Increased credit utilization: Unpaid balances increase your credit utilization ratio, which negatively affects your CIBIL score if it exceeds 30%.

- Long-Term Impact: Frequent late credit card payments can lead to a “default” status, staying on your credit report for up to 7 years, making it tougher to procure loans or new credit cards.

Maintaining a CIBIL score of 750 or above is ideal for eligibility for IDFC First credit cards and other financial products. Timely IDFC First credit card payments are essential to keep your score intact.

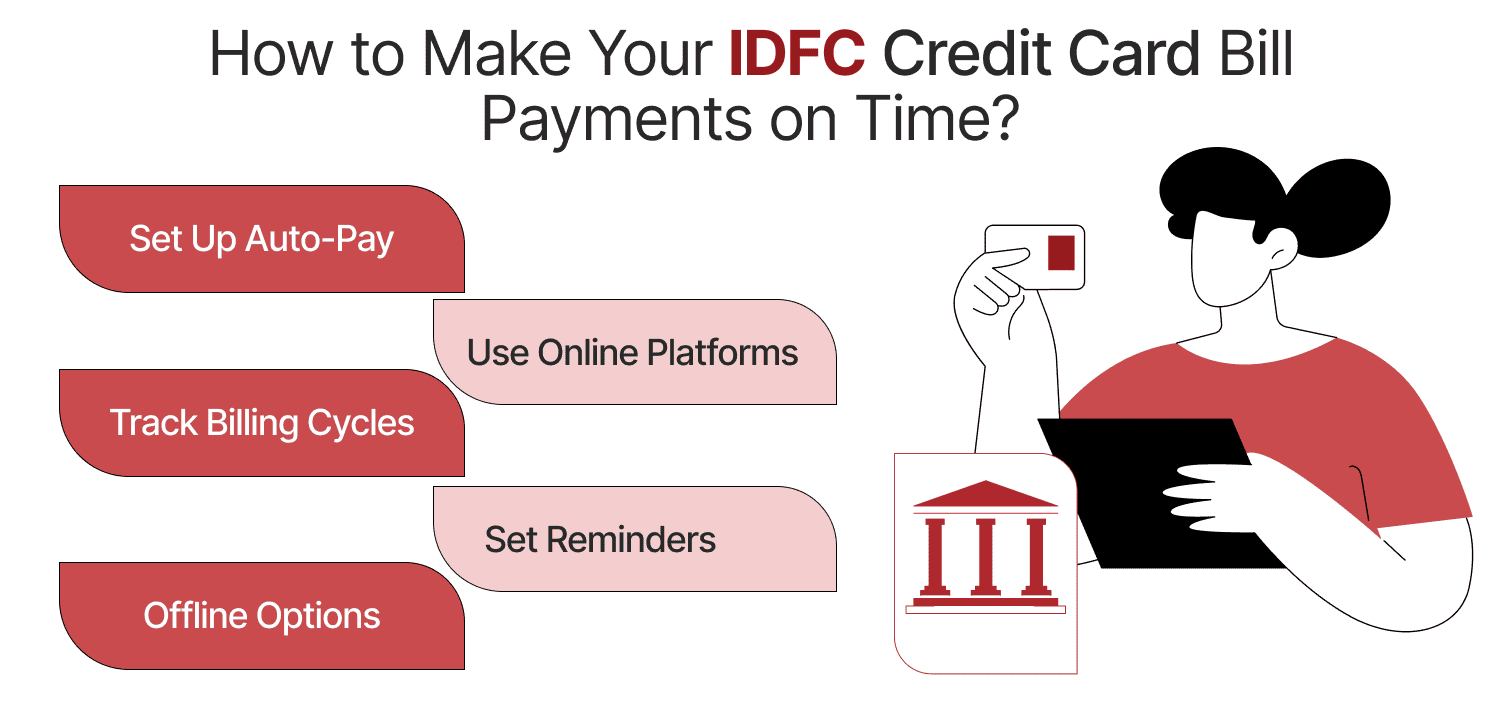

How to Make Your IDFC Credit Card Bill Payments on Time?

To avoid IDFC First Bank Credit Card Late Payment Charges, follow these steps to ensure timely IDFC First credit card payments:

- Set Up Auto-Pay: Log in to the IDFC First Bank mobile app or net banking portal, navigate to the “Credit Cards” section, and enable auto-pay for the minimum or total amount due. This guarantees automatic deductions from your linked bank account.

- Use Online Platforms: Pay your credit card bill via the Bajaj Finserv BBPS platform, IDFC First Bank’s website, or mobile app using UPI, net banking, debit/credit cards, or e-wallets.

- Track Billing Cycles: The IDFC credit card billing cycle typically spans 25–31 days. Check your statement or online account to know your cycle and due date (usually 21 days after the cycle ends).

- Set Reminders: Use calendar alerts or banking apps to remind you of your credit card payment due date.

- Offline Options: Visit an IDFC First Bank branch to pay via cash (₹100 processing fee applies) or drop a cheque with your 16-digit credit card number.

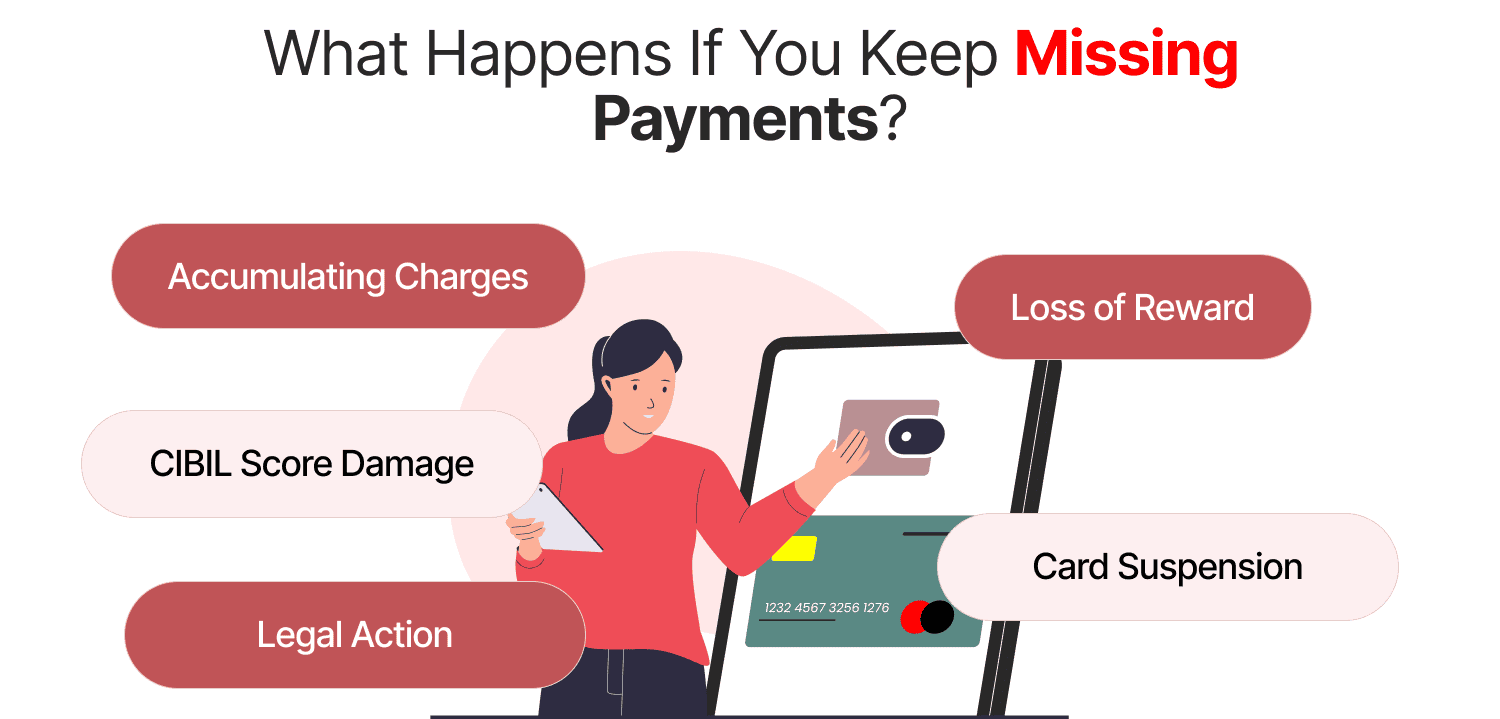

What Happens If You Keep Missing Payments?

Consistently missing IDFC First credit card payments can lead to severe consequences:

- Accumulating Charges: Each missed payment incurs IDFC First Bank Credit Card Late Payment Charges (up to ₹1,200) and interest, increasing your debt.

- CIBIL Score Damage: Multiple missed payments can drop your CIBIL score significantly, affecting future credit applications.

- Legal Action: Persistent non-payment may lead to recovery actions by the bank, including legal proceedings.

- Card Suspension: IDFC First Bank may suspend or cancel your credit card, limiting your access to credit.

- Loss of Rewards: Upon card closure due to non-payment, all accumulated reward points lapse, reducing the benefits of IDFC First credit cards.

Tips to Prevent IDFC Credit Card Late Payment Charges

Here are practical tips to avoid IDFC First Bank Credit Card Late Payment Charges:

- Budget Wisely: Track your spending to ensure you have funds for credit card payments. Use IDFC First Bank’s mobile app to monitor transactions.

- Pay more than the Minimum: Paying only the minimum amount outstanding enables you to avoid late fees. However, you will have to pay the interest accumulated on the outstanding balance. Aim to pay the complete balance.

- Use UPI for Quick Payments: Link your IDFC First credit card to UPI apps for fast, hassle-free payments. The FIRST SWYP Credit Card offers 100% cashback (up to ₹200) on the first four UPI transactions.

- Check Statements Regularly: Review your IDFC credit card statement to understand your spending and due dates.

- Contact Customer Support: If you foresee payment issues, contact IDFC First Bank’s customer service at 1800 10 888 to discuss payment plans.

How Do IDFC Credit Card Payments Impact Your CIBIL Score?

Timely IDFC First credit card payments positively impact your CIBIL score in several ways:

- Builds Credit History: Regular, on-time payments demonstrate reliability, boosting your CIBIL score over time.

- Lowers Credit Utilization: Paying off your balance reduces your credit utilization ratio, a key factor in your CIBIL score calculation.

- Avoids Negative Marks: Consistent credit card payments prevent late payment reports to credit bureaus, protecting your score.

Conversely, late or missed IDFC First credit card payments can lower your CIBIL score, increase your debt, and limit your eligibility for future credit cards or loans. For those who have a low CIBIL score, secured credit cards can be taken to enhance your credit history. You can build your credit score by paying your secured credit card bills on time. IDFC First Wow is a secured credit card which can be obtained against a fixed deposit.

Conclusion

Understanding and managing IDFC First Bank Credit Card Late Payment Charges is essential for financial health. By staying informed about your IDFC credit card billing cycle, setting up auto-pay, and monitoring your spending, you can avoid costly fees and maintain a strong CIBIL score. IDFC First credit cards offer attractive benefits like lifetime-free usage, low interest rates, and evergreen reward points, but these perks are best enjoyed with disciplined credit card payments. Take control of your finances today by prioritizing timely IDFC First credit card payments and leveraging the bank’s flexible payment options.

Frequently Asked Questions (FAQs)