Best Investment Plans for Women

Last Updated : Sept. 24, 2024, 4:53 p.m.

Women manage monthly budgets so easily that no one has to worry about the same. And from that, a small amount is saved. Now, the question is – what should women do with that saved sum? Well, in times like this, making sound investments matters. And there are plenty of investment options women can choose from to achieve their financial goals. Both risk-oriented and fixed-return investment options are available. So which are the best investment plans for women from the available options? Let’s find out in the article below.

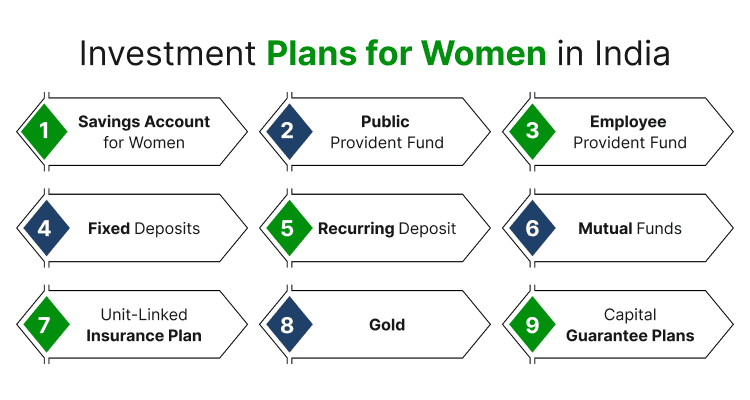

Investment Plans for Women in India

Women have become more stronger and self-reliant in society today owing to exciting job opportunities. And with the following investment plans, they can earn more.

Investment Option | Interest Rate / Returns | Benefits |

|---|---|---|

Varies by bank | High interest, discounts, cashback, exclusive privileges | |

7.1% per annum | Risk-free, tax benefits under Section 80C | |

Employee Provident Fund (EPF) | 8.25% per annum | Tax benefits, reduced contribution rate for new women employees |

Fixed Deposit (FD) | 3.00% to 8.00% | Stable returns, no market risk, flexible tenure |

Recurring Deposit (RD) | 5% to 7.5% per annum | Encourages disciplined saving, low-risk investment |

Mutual Funds | Varies | High return potential, diversification to manage risk |

Depends on fund performance | Protects family, loyalty additions, partial withdrawals | |

Gold | Varies | Hedge against inflation, financial security |

Capital Guarantee Plans | Fixed-rate of return | Low risk, suitable for short-term goals |

Savings Account for Women

Banks like HDFC, ICICI, IDFC, and more provide specially designed savings accounts for women . Well, you must be thinking about how it is different from a regular savings account . In this, you’ll get –

- High Interest

- Discounts

- Cashback

- Other exclusive privileges

And this is the first and foremost investment plan that can come to one’s head. So, if you want to play safe with your investment, open a women’s savings account.

Public Provident Fund (PPF)

This is a savings cum tax benefit investment plan where you’ll get more interest than the savings account. Currently, the interest is 7.1% per annum on PPF. Using this investment plan, you can build a corpus for your retirement. And you can begin investing with a minimum of INR 500. The maximum investment is INR 1.5 lakh a year in PPF.

This is a risk-free investment option wherein you can earn tax benefits under section 80C of the Income Tax Act.

Employee Provident Fund (EPF)

EPF is a retirement scheme for employees working in the government or private sector. In this, a portion of your income is invested in the EPF account wherein an interest of 8.25% per annum is available.

In a bid to promote higher employment among women, the government has reduced the EPF contribution rate for new women employees to 8% for the first three years of their employment, compared to the standard rate of 12%. This reduction allows women to take home a higher salary while still contributing to their retirement savings.

Women can make partial withdrawals from their EPF account for various reasons such as medical treatment, marriage, and education of children.

Fixed Deposit (FD)

This is a reliable savings scheme for women looking to grow their funds securely. By investing your money for a set period, you earn a steady interest rate. The FD rate ranges from 3.00% to 8.00% based on your deposit amount and chosen tenure.

You can invest up to 10 years in fixed deposits And there is no risk of market fluctuations, so you can get the desired amount at the end of the tenure. You can use the FD calculator and find the expected outcome.

For instance, Neha is looking to invest some money in a fixed deposit. She uses the ICICI Bank FD Calculator to find the possible return –

- Investment amount – INR 25,000

- Tenure – 5 years

The applicable interest rate is up to 6.80%. So, by March 2027, Neha will get an amount of INR 34,737.

Recurring Deposit (RD)

It is an excellent savings option for women investors looking for a financial cushion over time. This scheme allows you to save a fixed amount of money regularly - usually monthly - over a predetermined period. This helps to manage your finances easily and encourages disciplined saving. The interest rates for recurring deposits typically range from 5% to 7.5% per annum, depending on the bank and the tenure chosen. Additionally, RDs are low-risk investments, providing a safe and predictable return on your savings.

Mutual Fund

There is a wide range of mutual funds available in the market, offering the potential for high returns on your investments. Equities, while offering high returns, also carry higher risks. Equity funds could be the best investment plans for women who are willing to take more risks for higher returns. For investors with medium to high-risk appetites, a hybrid fund, which mixes equity and debt investments, may be more suitable.

In a hybrid fund, a portion of your investment goes into equities, while the remainder is invested in debt instruments. This diversification means that if the market declines, your losses may be mitigated. For those new to mutual funds, investing in debt funds can be a more secure option and provide a good opportunity to learn about market movements. So, how can you invest in mutual funds? You can invest directly through an asset management company (AMC) or distributors affiliated with them.

Unit-linked Insurance Plan

This is a life insurance cum investment plan where women can protect their families and also invest money to build a corpus by the end of the policy period. If the insured passes away, the insurance company pays a death benefit to the nominee, which ranges from INR 10 lakh to INR 1 crore, depending on the sum insured. The policyholder can choose from different funds based on their financial goals and the level of risk they are willing to take. Accordingly, a portion of your premium will be invested in the chosen fund.

During the tenure, the insured will get the following benefits –

- Loyalty additions – The company will invest a percentage of the premium amount in your chosen fund. And this will enhance your outcome.

- Partial withdrawal facility – In case of a financial emergency, you can withdraw units from your fund. This facility is available after five consecutive policy years.

Gold

Gold has always been seen as a safe and excellent investment choice for women in India. Women can invest in gold in different ways, such as buying physical gold (like jewelry or coins), gold ETFs (Exchange Traded Funds), or sovereign gold bonds.

Investing in gold can protect against inflation and provide financial security, making it a valuable part of any investment portfolio.

Capital Guarantee Plans

Capital guarantee plans are investment products that promise to return your initial investment amount at maturity, no matter how the market performs. This feature provides reassurance, especially for those saving for short-term goals.

These plans typically offer a fixed rate of return, allowing you to expect steady growth and know what you will receive in the future.

They are perfect for individuals who prefer to take less risk and want to protect their capital. This is why capital guarantee plans are seen as one of the best investment options for women.

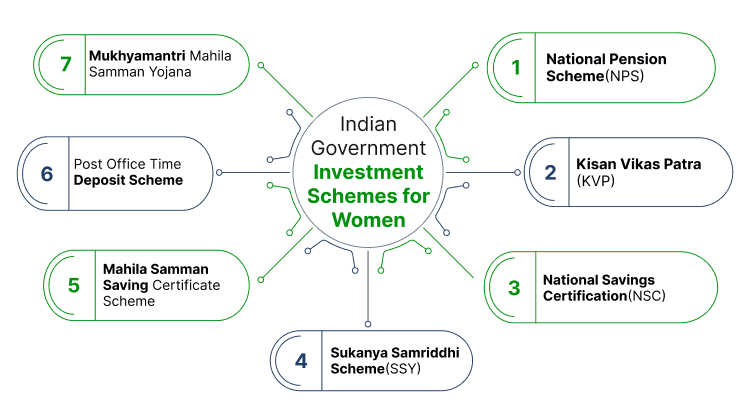

Indian Government Investment Schemes for Women

The Indian government provides a range of investment schemes aimed at financially empowering women. Here are some of the best saving options for women:

Investment Scheme | Key Features | Interest Rate / Returns | Eligibility |

|---|---|---|---|

Two accounts: Tier I (mandatory) and Tier II (voluntary) with tax benefits | 9% to 12% | Tier I: Aged 18 to 65; Tier II: Existing Tier I holders | |

Doubles investment in 124 months, no upper limit on investment | Returns vary (doubling effect) | Minimum investment: ₹1,000 | |

National Savings Certificate (NSC) | Secure investment through post offices | 6.80% | Minimum investment: ₹1,000; lock-in period: 5 years |

Promotes education and financial security for girl children | 8.20% | Account for girl children under 10 years | |

Small savings scheme for women or girl children, one-time investment | 7.50% | Minimum investment: ₹1,000; max: ₹2 lakh; withdrawal after 1 year | |

Post Office Time Deposit Scheme | Safe investment option with guaranteed returns | 6% to 7.5% | Minimum deposit: ₹200; duration: 1 to 5 years |

Mukhyamantri Mahila Samman Yojana | Monthly assistance program for women aged 18 and older | ₹1,000 per month | Must have a voter ID card in Delhi |

National Pension Scheme (NSP)

It is a government-supported scheme that provides a secure and long-term investment solution for retirement planning. NPS offers two types of accounts -

- Tier I: It is a mandatory retirement savings account that you cannot access until you retire.

- Tier II: It is a voluntary savings account that allows for easier withdrawals.

You can get tax benefits on contributions made under Section 80CCD (up to ₹1.5 lakhs). This can lower your tax bill and help you save more for retirement. Also, you can earn an interest rate, ranging from 9 to 12%.

For a better understanding, please refer to the table below:

Criteria | Tier I | Tier II |

|---|---|---|

Eligibility | Any Indian citizen aged 18 to 65 | Existing Tier I account holders only |

Lock-in Period | Until the age of 60 | None |

Number of Yearly Deposits | Minimum of 1 deposit per year | Yearly deposits are optional |

Minimum Contribution | ₹500 | ₹250 |

Tax Benefits | Tax exemption under Section 80CCD (1) for up to ₹1.5 lakhs, plus additional deductions up to ₹50,000 under Section 80CCD (1B) | No tax benefits |

Kisan Vikas Patra

It is a small savings account introduced by the Indian Post Office to double your investment over 124 months. You can invest a minimum of INR 1,000 in this. There is no upper limit for investment in the scheme. Types of Kisan Vikas Patra Certificate –

- Single Holder – This is issued to an adult for self or on behalf of a minor

- Joint ‘A’ – For two adults, and here, the amount is payable to both the holders jointly or to the one who is alive till the end of the term.

- Joint ‘B’ – For two adults, and in this, the amount is payable either to the holders or the one who survives.

National Savings Certificate (NSC)

This is a secure investment option provided by the government of India through post offices that offer 6.8% interest on your investment. You can start with a minimum of INR 1,000. This savings product comes with a lock-in period of five years. It is a low-risk investment for women and helps them earn steadily.

You can visit any nearest post office branch to get NSC. It also offers tax benefits, as the interest earned on EPF contributions is eligible for deductions under Section 80C of the Income Tax Act.

Sukanya Samriddhi Scheme

The Sukanya Samriddhi Yojana (SSY) is a government-backed scheme aimed at promoting the education and financial security of girl children. Parents or guardians can open an account for a girl child under 10 years old.

This scheme offers higher interest rates than regular savings accounts, currently at 8.2% per annum. Additionally, the money deposited in SSY qualifies for tax deductions under Section 80C of the Income Tax Act. This makes it an excellent long-term investment for a girl child’s education or wedding expenses. A girl child is eligible to have only one SSY account. It can be opened at any post office or approved branch of a commercial bank.

Mahila Samman Saving Certificate Scheme

It is a small savings scheme backed by the government that can be opened in the name of a girl child or woman. This is a one-time scheme available for two years - April 2023 to March 2025. It offers a fixed interest rate of 7.5% per annum.

You can invest a minimum of ₹1,000 and a maximum of ₹2 lakh in this scheme. The account holder can withdraw up to 40% of the account balance after one year of opening the account.

Post Office Time Deposit Scheme

The Post Office Time Deposit (TD) Scheme, offered by the Indian post office, is a secure investment choice for women. It is designed for those looking for guaranteed returns on their investment over a fixed period.

The scheme offers fixed interest rates on deposits that range from 6% to 7.5% per annum, depending on the selected deposit duration. The duration can range from 1 to 5 years. You can start an account with a minimum deposit of ₹200 and make additional deposits in multiples of ₹200. There is no upper limit on the total investment.

Mukhyamantri Mahila Samman Yojana

Launched during the 2024 budget speech by the Delhi government, the Mukhyamantri Mahila Samman Yojana is a program to support women. It gives women aged 18 and older a monthly payment of ₹1,000. To qualify for this scheme, residents of Delhi need to have a voter ID card from the National Capital.

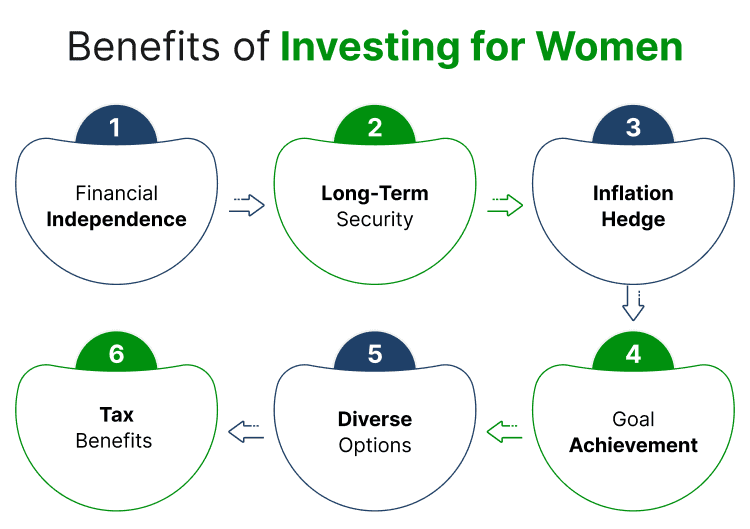

The Benefits of Investing for Women

Investing is a smart choice for women for several reasons, including the potential for wealth growth and increased financial independence. Here are some key reasons why investing is beneficial for women:

- Financial Independence : Investing helps women build their wealth, providing greater financial independence. This empowers them to make choices that align with their personal and professional goals.

- Long-Term Security : Investments can provide long-term financial security, which is especially important for women who may live longer than men. Building a substantial investment portfolio helps ensure a comfortable retirement.

- Inflation Hedge : Investing can help combat inflation. While savings accounts may not keep up with rising costs, investments in stocks, mutual funds, or real estate can offer returns that outpace inflation.

- Goal Achievement : Whether it's saving for a child's education, buying a home, or starting a business, investing allows women to grow their savings over time and achieve their financial goals.

- Diverse Options : Women can choose from a wide range of investment options, including stocks, bonds, mutual funds, and real estate, allowing them to tailor their investment strategy to their risk tolerance and financial objectives.

- Tax Benefits : Many investment options come with tax advantages, helping women save more effectively and keep more of their earnings.

Wrapping Up!

Before investing your hard-earned money, it’s important to do thorough market research and choose the investment option that fits your risk level. There are many other investment schemes available for women in India that range from low to high risk. Every woman should take charge of her financial decisions and select options that will help her grow both financially and personally in the future.

Frequently Asked Questions (FAQs)